Annual Reports

FinVolution Group's annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

FinVolution Group — FY2025 Annual Report (Form 20-F) — FY2025

Management's fullest account of a China-plus-overseas online lender whose 'capital-light' model still bears the credit risk it facilitates, run through a Cayman/VIE structure. · Open the full document →

Item 3.D. Risk Factors — We bear credit risk for the majority of loans funded by our institutional funding partners — p. 35 · Read the full section →

The crux of the model: despite the 'capital-light' framing, quality-assurance commitments leave FinVolution holding the default risk on most facilitated loans.

Quality-assurance commitments put credit risk back on FinVolution for a majority of the loans it facilitates.

We provide our institutional funding partners with quality assurance commitments for a majority of the loans they have funded. […] As a result, we are subject to credit risk for such loans. […] Any deterioration in our loan portfolio quality and increase in default risks could materially adversely affect our results of operations.

p. 35 · Read in context →

Item 3.D. Risk Factors — Risks Related to Our Corporate Structure (the VIE arrangements) — p. 51 · Read the full section →

The whole China business is consolidated through contracts, not ownership; if Beijing rejects the VIE structure the group could lose its operating entities.

The company concedes it cannot assure that regulators will accept the VIE contracts, and lists what a rejection could trigger.

Although we believe we, our PRC subsidiaries and the consolidated variable interest entities comply with current PRC laws and regulations, we cannot assure you that the PRC government would agree that our contractual arrangements comply with PRC licensing, registration or other regulatory requirements […] If the PRC government determines that we or the consolidated variable interest entities do not comply with applicable law, it could revoke the consolidated variable interest entities’ business and operating licenses, require the consolidated variable interest entities to discontinue or restrict the consolidated variable interest entities’ operations, restrict the consolidated variable interest entities’ right to collect revenues

p. 52 · Read in context →

Item 4. Information on the Company — B. Business Overview — p. 75 · Read the full section →

How the platform actually works: who it lends to, the 2020 pivot from balance-sheet lender to technology enabler, and how the capital-light fee is earned.

What the business is — a young-borrower-focused fintech spanning China and overseas markets.

We are a leading fintech platform with strong brand recognition across China and key overseas markets. Launched in 2007, we have been a pioneer in China’s online consumer finance industry. […] We strategically focus on serving borrowers of the young generation that is typically more receptive to internet financial services and whose borrowing needs are unserved or underserved by traditional financial institutions.

p. 75 · Read in context →

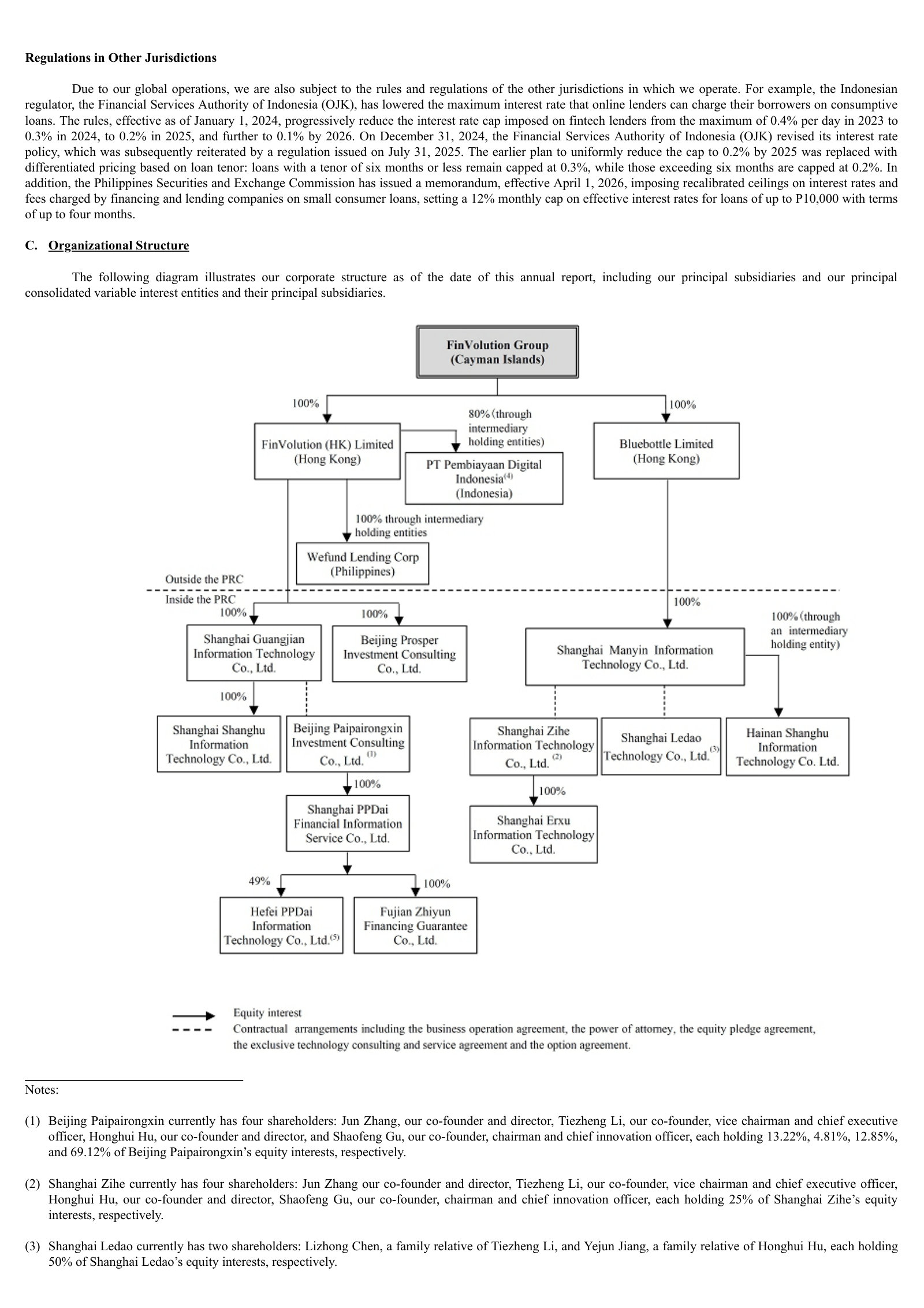

Item 4. Information on the Company — C. Organizational Structure — p. 101 · Read the full section →

The map of the Cayman parent, Hong Kong intermediaries, PRC subsidiaries and the consolidated VIEs — the structure behind the corporate-structure risk.

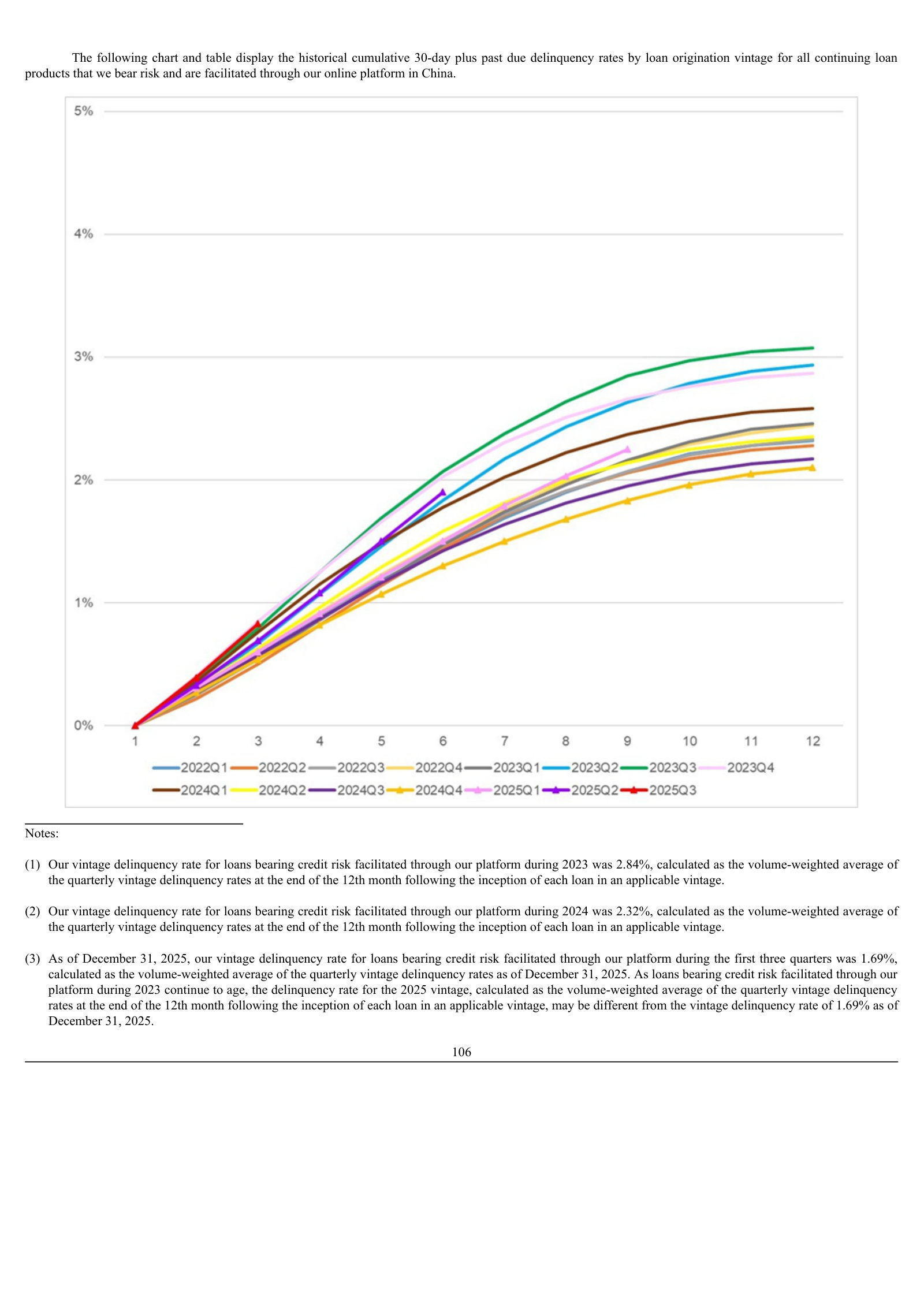

Item 5.A. Operating Results — Loan Performance Data — p. 111 · Read the full section →

For a lender, credit quality is the number that matters; the vintage curves show how risk-bearing China loans have seasoned across cohorts.

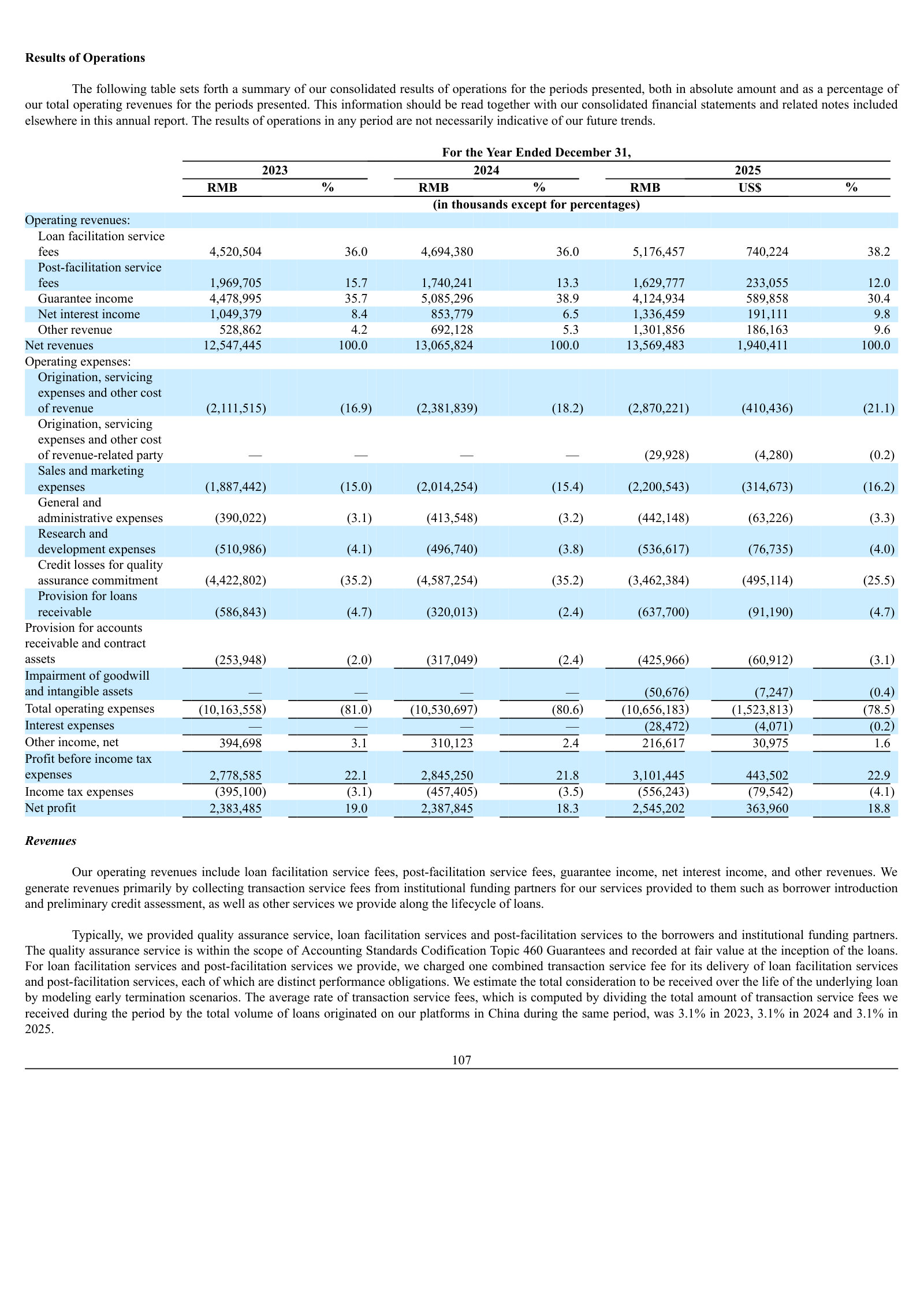

Item 5.A. Operating Results — Results of Operations — p. 113 · Read the full section →

Where management explains the revenue mix and what moved it — the shift from guarantee income toward facilitation and net interest income.

Note 2(s). Quality Assurance Obligations (Significant Accounting Policies) — p. 189 · Read the full section →

The accounting policy that defines the model: it converts the guarantee into deferred income and a credit-loss liability, which is why 'capital-light' still carries risk.

How the guarantee works and how it is booked — compensation obligation on default, income released as risk runs off.

For off-balance sheet loans funded by institutional funding partners, the Group provides quality assurance commitment to compensate them in the event of borrowers’ default […] the Group is obligated to compensate the third-party guarantee companies at an amount equal to the repayment made to the institutional funding partners. […] deferred guarantee income is released systematically as guarantee income in revenue in the consolidated statement of comprehensive income as the Group is released from the underlying risk.

p. 189 · Read in context →

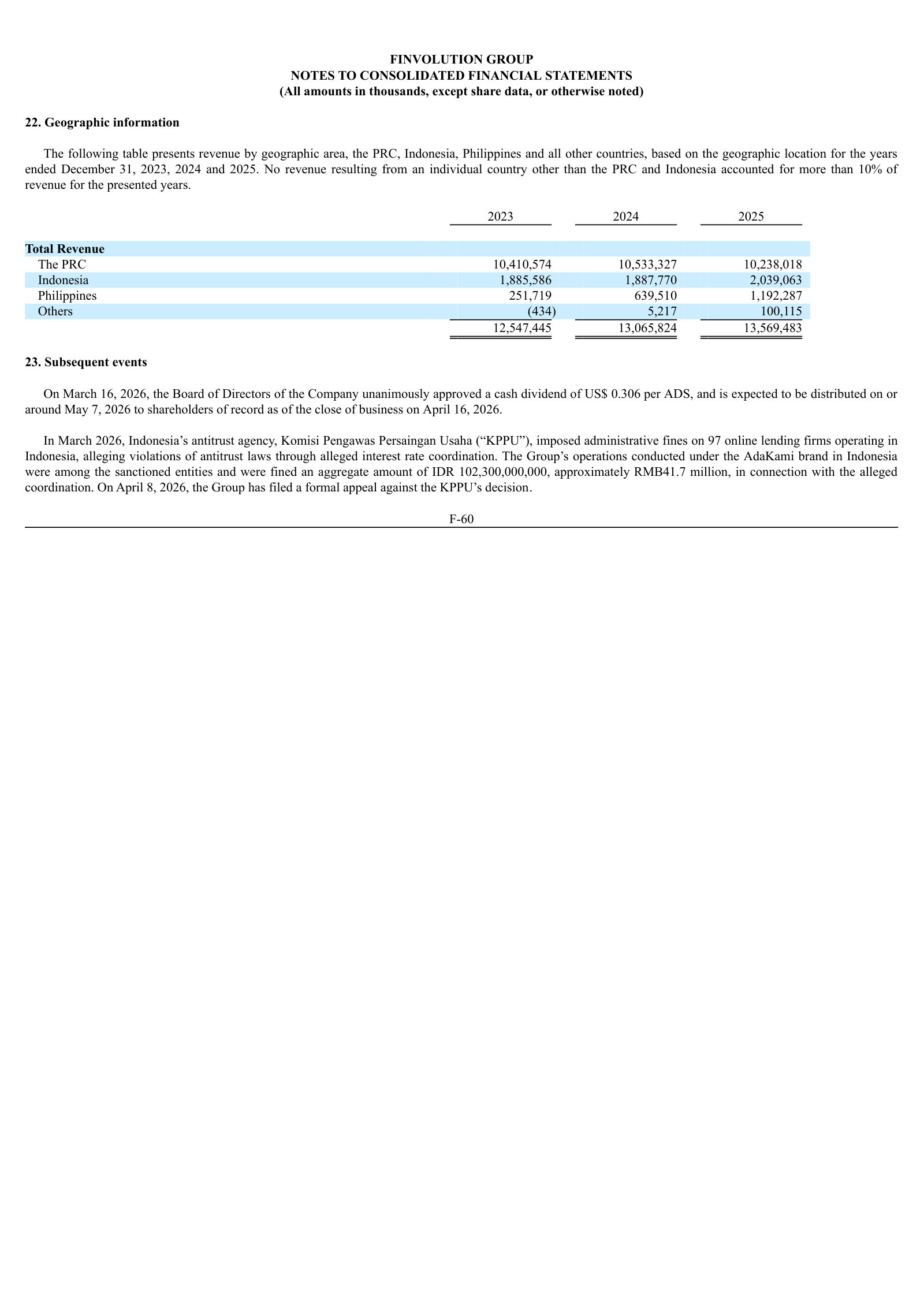

Note 22. Geographic Information — p. 221 · Read the full section →

The segment split in one table — China still ~75% of revenue while Indonesia and the Philippines scale; note the KPPU fine flagged just below.

More annual reports

FinVolution Group — FY2024 Annual Report (Form 20-F) — FY2024 · 260 pages · The year overseas expansion accelerated and the Indonesian multi-finance acquisition began — a useful baseline for the FY2025 international story. · Open →

FinVolution Group — FY2023 Annual Report (Form 20-F) — FY2023 · 215 pages · Shows the model mid-transition, with China still dominant before overseas revenue reached a quarter of the total. · Open →

FinVolution Group — FY2022 Annual Report (Form 20-F) — FY2022 · 273 pages · Captures the post-capital-light-pivot period and the earlier PRC regulatory tightening on online consumer lending. · Open →

FinVolution Group — FY2021 Annual Report (Form 20-F) — FY2021 · 270 pages · The earliest edition on the shelf — the capital-light model still new and China essentially the entire business. · Open →