Full Report

The numbers behind FinVolution Group: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in RMB thousands unless noted.

Reading notes: All figures are in thousands of Renminbi (RMB) exactly as printed on the face of FinVolution's SEC filings (Form 20-F annual reports and quarterly earnings releases), which report in RMB with a supplemental US$ convenience-translation column that is not used here. The company is a Cayman-incorporated foreign private issuer filing under U.S. GAAP; its ADSs trade on the NYSE (one ADS = five Class A ordinary shares). Each of FY2021-FY2025 is cited to that fiscal year's own Form 20-F (current-year column). FY2019 and FY2020 figures in the Long-Term Record are the comparative columns of the FY2021 Form 20-F. Revenue is shown two ways: by product/service line (loan facilitation fees, post-facilitation fees, guarantee income, net interest income, other) from the face of the income statement, and by geography (the PRC, Indonesia, Philippines, others) from the Geographic information note. The Philippines was disclosed separately only from FY2023; in FY2021-FY2022 it is included within 'Others'. The FY2021 balance-sheet line 'Liability from quality assurance commitment' was captioned 'Expected credit losses for quality assurance commitment' in the FY2021 Form 20-F; the label was standardized here.

Share Price — Full Available History — 9 Years

The stock closed at $4.78 on Jul 16, 2026 — down 63% over the window shown (-10.9% a year), trading between $1.30 and $13.15.

Source: market price feed, weekly closes, sampled from 2,180 source observations, Nov 2017–Jul 2026. Price return only, excludes dividends.

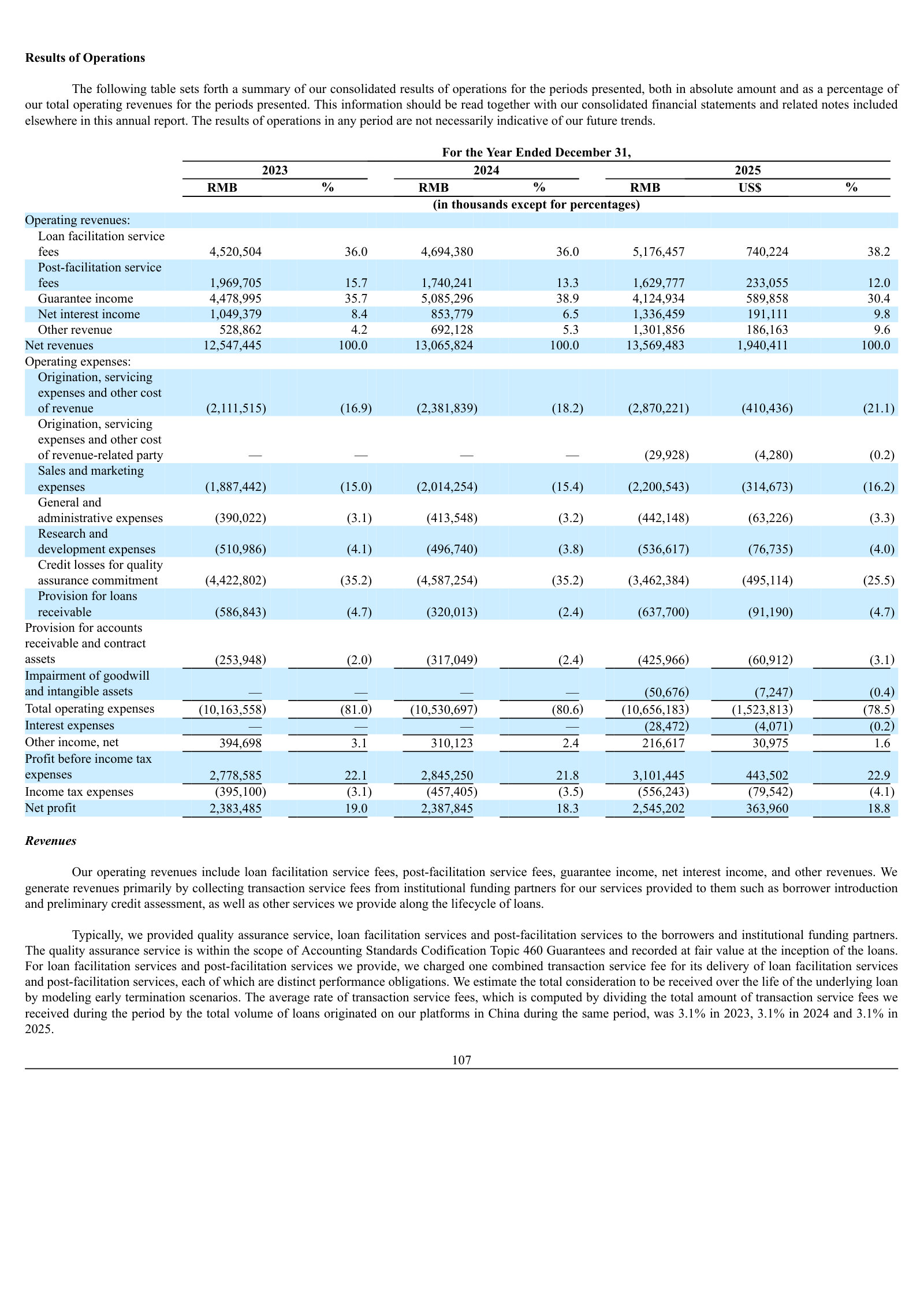

FY2025 at a Glance

Revenue (RMB thousands)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Net Revenue by Product

| Net Revenue by Product | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Loan facilitation service fees | 3,794,182 | 4,430,778 | 4,520,504 | 4,694,380 | 5,176,457 |

| Post-facilitation service fees | 1,309,565 | 1,929,913 | 1,969,705 | 1,740,241 | 1,629,777 |

| Guarantee income | 2,593,512 | 3,064,440 | 4,478,995 | 5,085,296 | 4,124,934 |

| Net interest income | 1,216,170 | 1,174,204 | 1,049,379 | 853,779 | 1,336,459 |

| Other revenue | 556,699 | 534,868 | 528,862 | 692,128 | 1,301,856 |

| Net revenues | 9,470,128 | 11,134,203 | 12,547,445 | 13,065,824 | 13,569,483 |

| Net revenues growth, derived | — | +17.6% | +12.7% | +4.1% | +3.9% |

Source: Consolidated Statements of Comprehensive Income - operating revenue lines [1] [2] [4] [5]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Comprehensive Income [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-16. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [6] [7] [8] [9]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [10] [11] [12] [13]. Click any linked figure to open the filing page with the row highlighted.

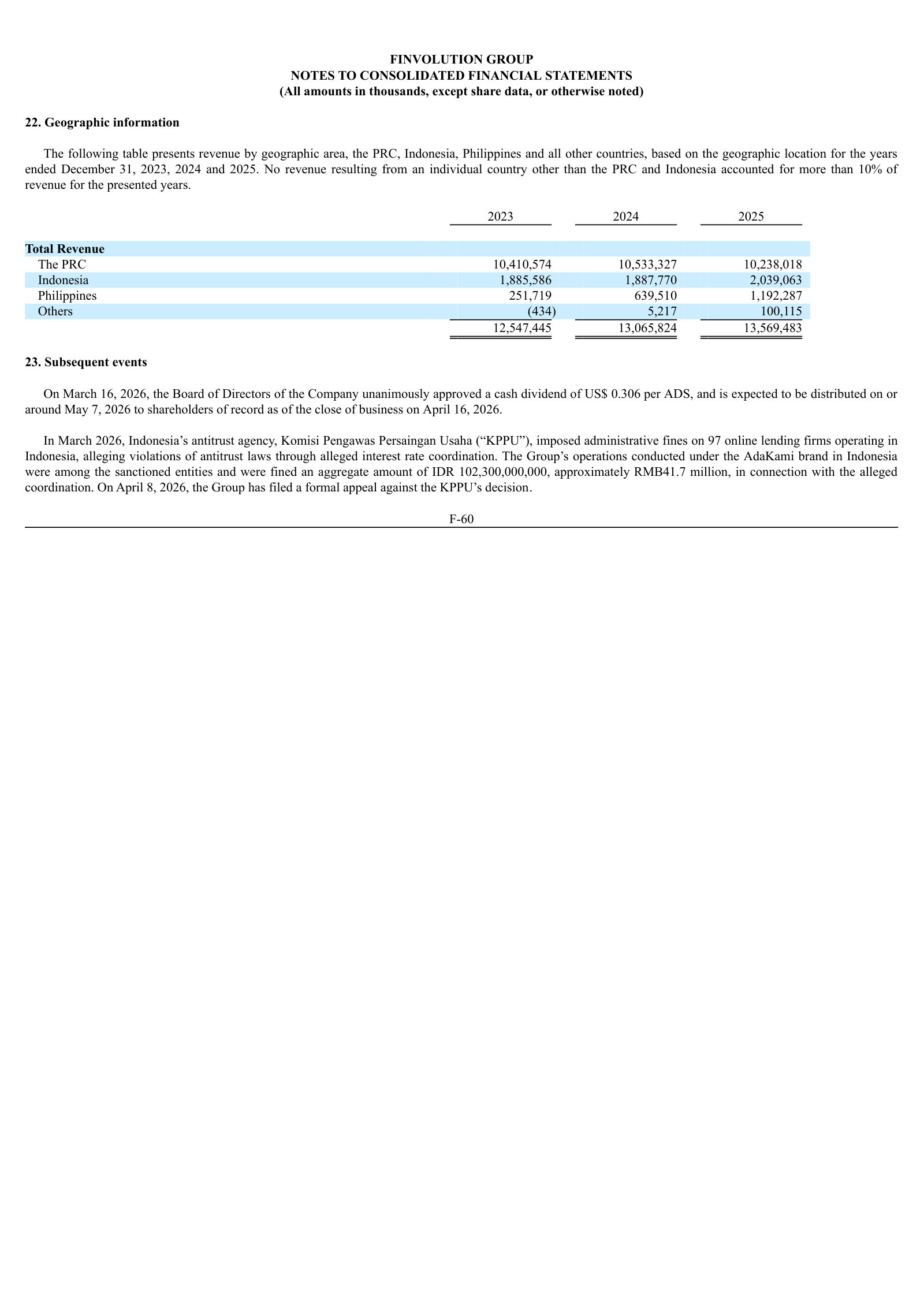

Net Revenue by Geography

| Net Revenue by Geography | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| The PRC | 8,643,683 | 9,984,500 | 10,410,574 | 10,533,327 | 10,238,018 |

| Indonesia | 701,642 | 1,067,429 | 1,885,586 | 1,887,770 | 2,039,063 |

| Philippines | — | — | 251,719 | 639,510 | 1,192,287 |

| Others | 124,803 | 82,274 | (434) | 5,217 | 100,115 |

| Total revenue | 9,470,128 | 11,134,203 | 12,547,445 | 13,065,824 | 13,569,483 |

Source: Form 20-F financial statement notes - Geographic information [14] [15]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Net profit attributable to FinVolution Group | Diluted net profit per ADS | Net cash provided by operating activities |

|---|---|---|---|---|

| FY2019 | 5,962,757 | 2,372,850 | 7.64 | (215,522) |

| FY2020 | 7,563,087 | 1,972,700 | 6.61 | 2,206,909 |

| FY2021 | 9,470,128 | 2,508,947 | 8.46 | 630,227 |

| FY2022 | 11,134,203 | 2,266,382 | 7.79 | 268,833 |

| FY2023 | 12,547,445 | 2,340,835 | 8.34 | 1,413,423 |

| FY2024 | 13,065,824 | 2,383,146 | 9.03 | 2,893,160 |

| FY2025 | 13,569,483 | 2,542,405 | 9.59 | 1,867,600 |

Source: consolidated statements across filings; older years from the standardized feed [11] [1] [13] [2]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-16. Estimate figures link to the consensus source, not to filing pages.

Traceability

366 of 366 figures on this page (100%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

All figures are in thousands of Renminbi (RMB) exactly as printed on the face of FinVolution's SEC filings (Form 20-F annual reports and quarterly earnings releases), which report in RMB with a supplemental US$ convenience-translation column that is not used here. The company is a Cayman-incorporated foreign private issuer filing under U.S. GAAP; its ADSs trade on the NYSE (one ADS = five Class A ordinary shares).

Each of FY2021-FY2025 is cited to that fiscal year's own Form 20-F (current-year column). FY2019 and FY2020 figures in the Long-Term Record are the comparative columns of the FY2021 Form 20-F.

Revenue is shown two ways: by product/service line (loan facilitation fees, post-facilitation fees, guarantee income, net interest income, other) from the face of the income statement, and by geography (the PRC, Indonesia, Philippines, others) from the Geographic information note. The Philippines was disclosed separately only from FY2023; in FY2021-FY2022 it is included within 'Others'.

The FY2021 balance-sheet line 'Liability from quality assurance commitment' was captioned 'Expected credit losses for quality assurance commitment' in the FY2021 Form 20-F; the label was standardized here.

The unaudited quarterly block (Q1 FY2025-Q1 FY2026) is taken from FinVolution's quarterly earnings-release financial statements; single-quarter income, point-in-time balance sheet, and single-quarter cash-flow figures are each cited directly to the release that printed them.

4 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

FinVolution Group's management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Presentation — Q4 2025 / Full-Year 2025 — Q4 & FY2025

The newest and fullest deck: the three-country franchise, the growth strategy, the operating engine, risk and capital returns — a company overview in one document. · Open the full document →

Investor Presentation — Q3 2025 — Q3 2025

Featured for four explanatory slides the newest deck dropped — how the loan-facilitation model actually works, the market-penetration case, and the addressable market. · Open the full document →

More from management

Investor Presentation — Q2 2025 — Q2 2025 · 27 pages · The mid-2025 interim data point, for readers tracking the quarter-by-quarter progression before the Q3 and full-year decks. · Open →

Investor Presentation — Q4 2024 / Full-Year 2024 — Q4 & FY2024 · 24 pages · The prior full-year review, with an explicit revenue-model slide (fees from funding partners) and leverage/liquidity detail the 2025 decks trimmed. · Open →

Investor Presentation — Q4 2022 / Full-Year 2022 — Q4 & FY2022 · 24 pages · The earliest deck on file, carrying a per-RMB100 unit-economics slide and balance-sheet detail that later editions dropped. · Open →

FinVolution Group's annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

FinVolution Group — FY2025 Annual Report (Form 20-F) — FY2025

Management's fullest account of a China-plus-overseas online lender whose 'capital-light' model still bears the credit risk it facilitates, run through a Cayman/VIE structure. · Open the full document →

Item 3.D. Risk Factors — We bear credit risk for the majority of loans funded by our institutional funding partners — p. 35 · Read the full section →

The crux of the model: despite the 'capital-light' framing, quality-assurance commitments leave FinVolution holding the default risk on most facilitated loans.

Quality-assurance commitments put credit risk back on FinVolution for a majority of the loans it facilitates.

We provide our institutional funding partners with quality assurance commitments for a majority of the loans they have funded. […] As a result, we are subject to credit risk for such loans. […] Any deterioration in our loan portfolio quality and increase in default risks could materially adversely affect our results of operations.

p. 35 · Read in context →

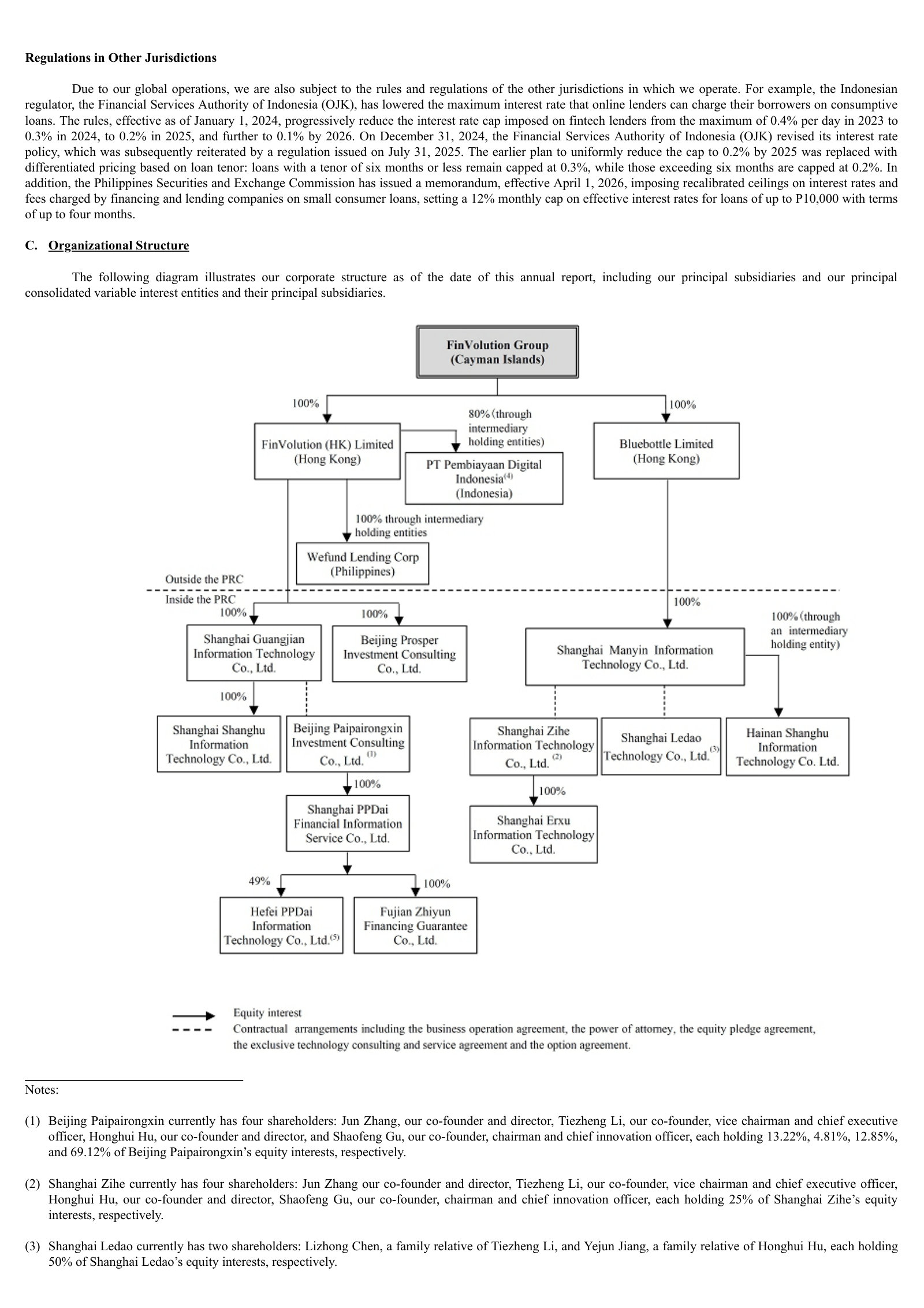

Item 3.D. Risk Factors — Risks Related to Our Corporate Structure (the VIE arrangements) — p. 51 · Read the full section →

The whole China business is consolidated through contracts, not ownership; if Beijing rejects the VIE structure the group could lose its operating entities.

The company concedes it cannot assure that regulators will accept the VIE contracts, and lists what a rejection could trigger.

Although we believe we, our PRC subsidiaries and the consolidated variable interest entities comply with current PRC laws and regulations, we cannot assure you that the PRC government would agree that our contractual arrangements comply with PRC licensing, registration or other regulatory requirements […] If the PRC government determines that we or the consolidated variable interest entities do not comply with applicable law, it could revoke the consolidated variable interest entities’ business and operating licenses, require the consolidated variable interest entities to discontinue or restrict the consolidated variable interest entities’ operations, restrict the consolidated variable interest entities’ right to collect revenues

p. 52 · Read in context →

Item 4. Information on the Company — B. Business Overview — p. 75 · Read the full section →

How the platform actually works: who it lends to, the 2020 pivot from balance-sheet lender to technology enabler, and how the capital-light fee is earned.

What the business is — a young-borrower-focused fintech spanning China and overseas markets.

We are a leading fintech platform with strong brand recognition across China and key overseas markets. Launched in 2007, we have been a pioneer in China’s online consumer finance industry. […] We strategically focus on serving borrowers of the young generation that is typically more receptive to internet financial services and whose borrowing needs are unserved or underserved by traditional financial institutions.

p. 75 · Read in context →

Item 4. Information on the Company — C. Organizational Structure — p. 101 · Read the full section →

The map of the Cayman parent, Hong Kong intermediaries, PRC subsidiaries and the consolidated VIEs — the structure behind the corporate-structure risk.

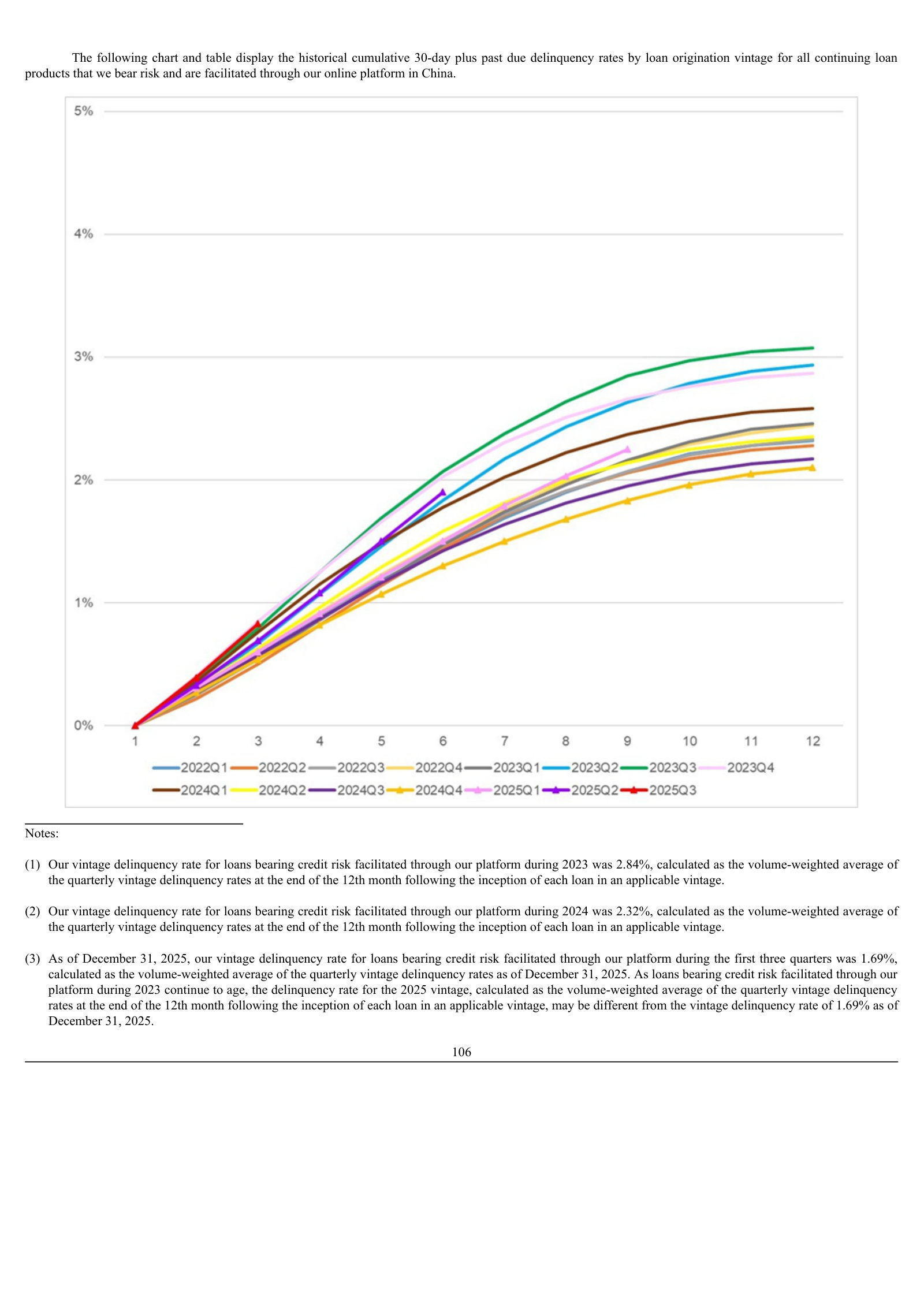

Item 5.A. Operating Results — Loan Performance Data — p. 111 · Read the full section →

For a lender, credit quality is the number that matters; the vintage curves show how risk-bearing China loans have seasoned across cohorts.

Item 5.A. Operating Results — Results of Operations — p. 113 · Read the full section →

Where management explains the revenue mix and what moved it — the shift from guarantee income toward facilitation and net interest income.

Note 2(s). Quality Assurance Obligations (Significant Accounting Policies) — p. 189 · Read the full section →

The accounting policy that defines the model: it converts the guarantee into deferred income and a credit-loss liability, which is why 'capital-light' still carries risk.

How the guarantee works and how it is booked — compensation obligation on default, income released as risk runs off.

For off-balance sheet loans funded by institutional funding partners, the Group provides quality assurance commitment to compensate them in the event of borrowers’ default […] the Group is obligated to compensate the third-party guarantee companies at an amount equal to the repayment made to the institutional funding partners. […] deferred guarantee income is released systematically as guarantee income in revenue in the consolidated statement of comprehensive income as the Group is released from the underlying risk.

p. 189 · Read in context →

Note 22. Geographic Information — p. 221 · Read the full section →

The segment split in one table — China still ~75% of revenue while Indonesia and the Philippines scale; note the KPPU fine flagged just below.

More annual reports

FinVolution Group — FY2024 Annual Report (Form 20-F) — FY2024 · 260 pages · The year overseas expansion accelerated and the Indonesian multi-finance acquisition began — a useful baseline for the FY2025 international story. · Open →

FinVolution Group — FY2023 Annual Report (Form 20-F) — FY2023 · 215 pages · Shows the model mid-transition, with China still dominant before overseas revenue reached a quarter of the total. · Open →

FinVolution Group — FY2022 Annual Report (Form 20-F) — FY2022 · 273 pages · Captures the post-capital-light-pivot period and the earlier PRC regulatory tightening on online consumer lending. · Open →

FinVolution Group — FY2021 Annual Report (Form 20-F) — FY2021 · 270 pages · The earliest edition on the shelf — the capital-light model still new and China essentially the entire business. · Open →

Competitors describe FinVolution Group's market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Qifu Technology, Inc. (QFIN)

The largest listed Chinese credit-tech loan-facilitation platform and FinVolution's most direct scale rival — same core model of matching consumer borrowers with institutional funding partners, and the benchmark for volume, borrower reach and embedded-finance distribution.

Qifu states its cumulative loan-facilitation scale and borrower base in China — the entrenched incumbent FinVolution competes against.

As of December 31, 2024, we had cumulatively facilitated approximately RMB2,212.0 billion (US$303.0 billion) of loans to 34.4 million borrowers. As of the same date, we had 56.9 million users with approved credit lines, accumulatively.

p. 123 · Read in context →

Qifu's reported annual facilitation volume, showing a decline across 2022–2024 — the sector-wide contraction in China's consumer-credit market that FinVolution also faces.

In 2024, we facilitated RMB322.0 billion (US$44.1 billion) of loans, representing a decrease from RMB369.1 billion in 2023 and RMB330.7 billion in 2022.

p. 206 · Read in context →

Qifu describes its 'embedded finance' distribution — routing credit through short-video, e-commerce, ride-hailing and smartphone platforms — the traffic-partnership acquisition model that collides with FinVolution's own.

In 2020, we started cooperating with leading online platforms with heavy user traffic under "embedded finance" model. These platform partners include, among others, leading short-form video platform, e-commerce platforms, ride hailing companies and smart phone companies. In 2024, we started to explore collaborations with financial institutions to engage their existing customer bases, leveraging their proprietary traffic alongside our differentiated pricing and service capabilities to expand the breadth and depth of our user coverage.

p. 135 · Read in context →

LexinFintech Holdings Ltd. (LX)

A direct Chinese consumer-finance rival (Fenqile/installment lending) with a large registered-user base and the same AI/big-data risk-and-facilitation model FinVolution runs, contesting the same borrowers and institutional funders.

LexinFintech states its registered-user and credit-line user base and its target demographic — the consumer-finance customer pool it contests with FinVolution.

As of December 31, 2023, the total number of our registered users reached 210 million, and users with credit line reached 42 million, among whom over 85% are aged between 23 and 40 years old and over 65% were urban working population. […] The number of our cumulative active users reached 31.1 million in 2023.

p. 142 · Read in context →

LexinFintech's self-description as 'a leading consumer finance technology company in China' resting on AI/big-data risk management — essentially the same positioning FinVolution claims.

We are a leading consumer finance technology company in China with a decade-long operating history. Upholding financial risk management as our operational cornerstone, we strive to apply advanced technologies such as AI and big data to form an online risk assessment and management system based on quantitative decision-making.

p. 136 · Read in context →

LexinFintech's stated institutional funding-partner count and outstanding funding balance — the bank/consumer-finance funding base both firms depend on.

We had cumulatively served over 170 funding partners as of December 31, 2024. The outstanding balance of funds provided by institutional funding partners was RMB125.6 billion and RMB114.1 billion (US$15.6 billion) respectively as of December 31, 2023 and December 31, 2024.

p. 141 · Read in context →

X Financial (XYF)

The closest structural twin to FinVolution's China business — a personal-finance loan-facilitation platform connecting prime/near-prime borrowers with institutional funders via proprietary big-data risk technology, at comparable annual volume.

X Financial describes its model — connecting borrowers with institutional funding partners through proprietary big-data technology — nearly identical to FinVolution's loan-facilitation model.

X financial is a leading online personal finance company in China. We are committed to connecting borrowers on our platform with institutional funding partners. With proprietary big data-driven technology, we have established strategic partnerships with financial institutions across multiple areas of its business operations, enabling us to facilitate loans to prime borrowers under a robust risk assessment and control system.

p. 124 · Read in context →

X Financial defines its target as 'prime borrowers underserved by traditional financial institutions' — the same near-prime segment FinVolution serves.

We strategically target the prime borrowers underserved by traditional financial institutions. We believe we set a high standard of credit quality by defining our borrowers as prime borrowers, who we define as an individual having sound credit history, who have credit records with PBOC CRC and usually no late payment record of over 60 days in the previous six months.

p. 126 · Read in context →

X Financial's cumulative and annual active-borrower counts — the customer base it has built in the market FinVolution also serves.

We facilitated loans to 16,309,242 active borrowers, each of whom made at least one transaction on our platform during the period from the commencement of our loan facilitation business to December 31, 2024. The number of our active borrowers increased from 3,326,774 in 2022 to 4,495,997 in 2023 and then further increased to 5,231,887 in 2024.

p. 128 · Read in context →

Yiren Digital Ltd. (YRD)

A direct Chinese loan-facilitation rival that also collides with FinVolution offshore — it names the Philippines (FinVolution's JuanHand market) as an expansion front — and frames the domestic market as consolidating toward a few national players.

Yiren Digital notes it is expanding financial services overseas 'such as in the Philippines,' facing regional peers — a direct collision with FinVolution's JuanHand operation there.

Meanwhile, as we expand our financial service businesses overseas, such as in the Philippines, we are facing competition from regional peers. For our insurance brokerage business, our company and the VIEs compete with other insurance brokerage companies in China. Given the overall low penetration rate of insurance services in China compared with the US and the Europe, we believe that our strategic deployment in insurance business has navigated us towards a large market with high growth potential.

p. 35 · Read in context →

Yiren Digital's stated view that tightening regulation and rising entry barriers have thinned the field to a few national players, 'leaving more market share opportunities' — the consolidation thesis FinVolution also invokes.

For our financial services business, our company and the VIEs compete with other consumer finance marketplaces and loan facilitation platforms that were intensely competitive before the year 2018. However, as the domestic regulations on the industry evolve and entry barriers continue to increase in recent years, fewer national-level players like us remain in the market while smaller platforms cease their operations, leaving more market share opportunities for us.

p. 35 · Read in context →

Jiayin Group Inc. (JFIN)

A direct Chinese loan-facilitation rival pursuing the same international runway as FinVolution — it established an Indonesia office to lead Southeast Asia growth, the market FinVolution serves through AdaKami.

Jiayin describes pushing beyond China into developing markets, citing its Indonesia office and Southeast Asia expansion — the same offshore strategy FinVolution runs through AdaKami.

While we operate our businesses with a focus on the China market, we have been exploring opportunities in other developing countries with a significant size of low- to mid- income population in recent years and intend to continue to expand our businesses in international markets. For example, we established our Indonesia office in 2019 to supervise our rapid development in Southeast Asia and we increased our investments in Indonesia in recent years to explore more business opportunities in local markets.

p. 52 · Read in context →

Jiayin's reported 2024 facilitation volume and funding-partner count — its scale in the Chinese loan-facilitation market alongside FinVolution.

In 2024, we and the VIE Group facilitated an aggregate loan volume of RMB100.8 billion (US$13.8 billion), funded by 48 institutional funding partners.

p. 197 · Read in context →

Lufax Holding Ltd (LU)

One of China's largest retail-credit and small-business-lending platforms (Ping An-affiliated). Its tilt toward small-business owners makes the consumer overlap partial, but it maps the competitive arena and runs the same guarantee-backed facilitation model FinVolution uses.

Lufax names its competitors — MYbank, WeBank, Du Xiaoman Financial and JD Technology, plus traditional banks — mapping the consumer- and small-business-credit arena FinVolution also operates in.

We face competition in the SBO financial services industry and the consumer finance industry. The SBO financial services industry and the consumer finance industry in China is becoming increasingly competitive. We compete primarily with non-traditional financial service providers such as MYbank, WeBank, Du Xiaoman Financial and JD Technology and with traditional financial institutions, such as traditional banks, which are focused on retail and SMB lending.

p. 45 · Read in context →

More peer documents

Qifu Technology Q1 FY2026 earnings call — 25 pages · CEO Haisheng Wu on China's soft consumer-credit demand and a fifth straight quarterly decline in household short-term loan balances (p5) — sector backdrop (note: OCR-noisy Motley Fool transcript). · Open →

X Financial FY2025 20-F — updated facilitation volume — 362 pages · Total loans facilitated rose to RMB130.6 billion in 2025 from RMB104.9 billion in 2024 (p106) — a scale update showing XYF re-accelerating. · Open →

Yiren Digital FY2025 20-F — updated scale — 252 pages · Borrowers served rose to ~14.3 million and 2025 facilitation to RMB67.8 billion (p82) — a scale update on the direct rival. · Open →

Jiayin Group Q4/FY2025 earnings call — 18 pages · Management cites ~187% YoY growth in Indonesia facilitation volume and ~119% user growth (p4) — quantifies the AdaKami-market collision (OCR-noisy transcript). · Open →

FinVolution at a glance

FinVolution Group is a profitable, cash-rich online consumer-finance platform that matches Chinese and Southeast-Asian borrowers with loans funded by banks and other institutions, taking a fee and standing behind most of the credit. It earned ¥2.5 billion (about US$364 million) on ¥13.6 billion of net revenue in 2025, holds more cash and investments than debt, and yet trades near a 52-week low at roughly 3.5 times earnings and about half of book value. This chapter establishes what the business is, how it makes money, and why the market prices it as a business in decline.

FinVolution reports in renminbi (¥). Dollar figures are the company's own period-end convenience translations from its Form 20-F; the ADS trades on the NYSE in US dollars, so market value, share price, and valuation multiples are shown in dollars. Ratios and percentages are unitless.

What the company does

FinVolution began as an online consumer-lending platform in June 2007 — among the first in China — and listed on the NYSE in November 2017 under its former name, PPDAI Group; it renamed to FinVolution in 2019 but still operates its Chinese platform under the PPDai brand [1]. It is not itself the lender of record for most of its volume. It runs the technology platform, acquires and underwrites the borrower, connects that borrower to an institutional funding partner, and services the loan — earning loan-facilitation fees, post-facilitation fees, and guarantee income rather than a pure interest spread [2].

The structure a shareholder actually owns is worth stating plainly at the outset. FinVolution is a Cayman Islands holding company with no equity in its Chinese operating entities; it consolidates them through contractual variable-interest-entity (VIE) arrangements, and those VIEs generated 71.1% of total revenue in 2025 [3]. Cash held inside the PRC is subject to transfer restrictions: net assets of ¥9.3 billion (US$1.3 billion) were restricted from distribution at the end of 2025 [4]. All four co-founders sit on the board; Shaofeng Gu is Chairman and Chief Innovation Officer, and co-founder Tiezheng Li is Vice Chairman and Chief Executive Officer [5].

The scale of the platform

Net revenue (¥bn, FY2025)

Net income (¥bn, FY2025)

Loans facilitated (¥bn, FY2025)

Registered users (m)

Sources: net revenue and net income, FY2025 20-F Consolidated Statements of Comprehensive Income [6]; loan volume and users, Item 4.B Business Overview [7].

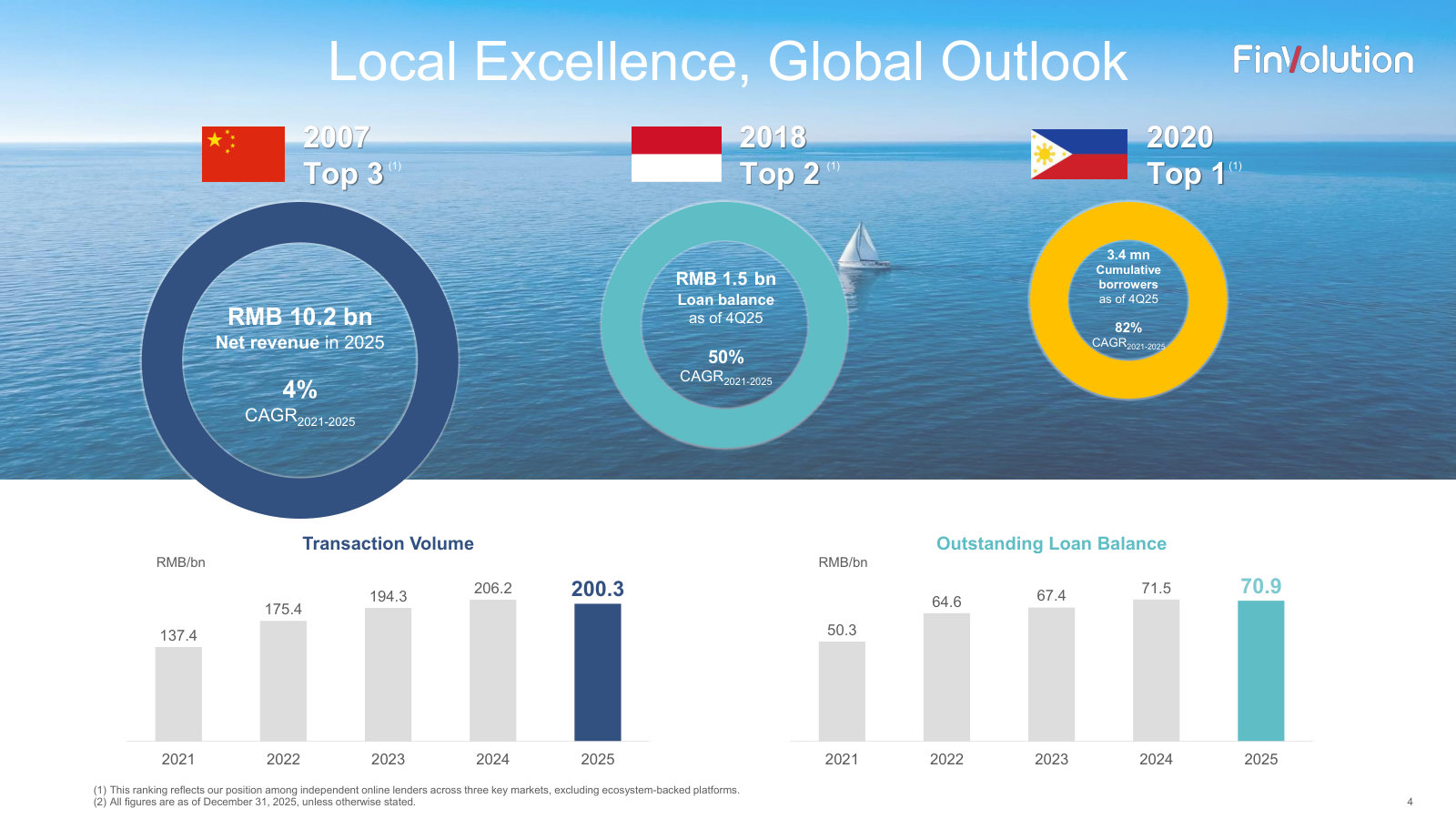

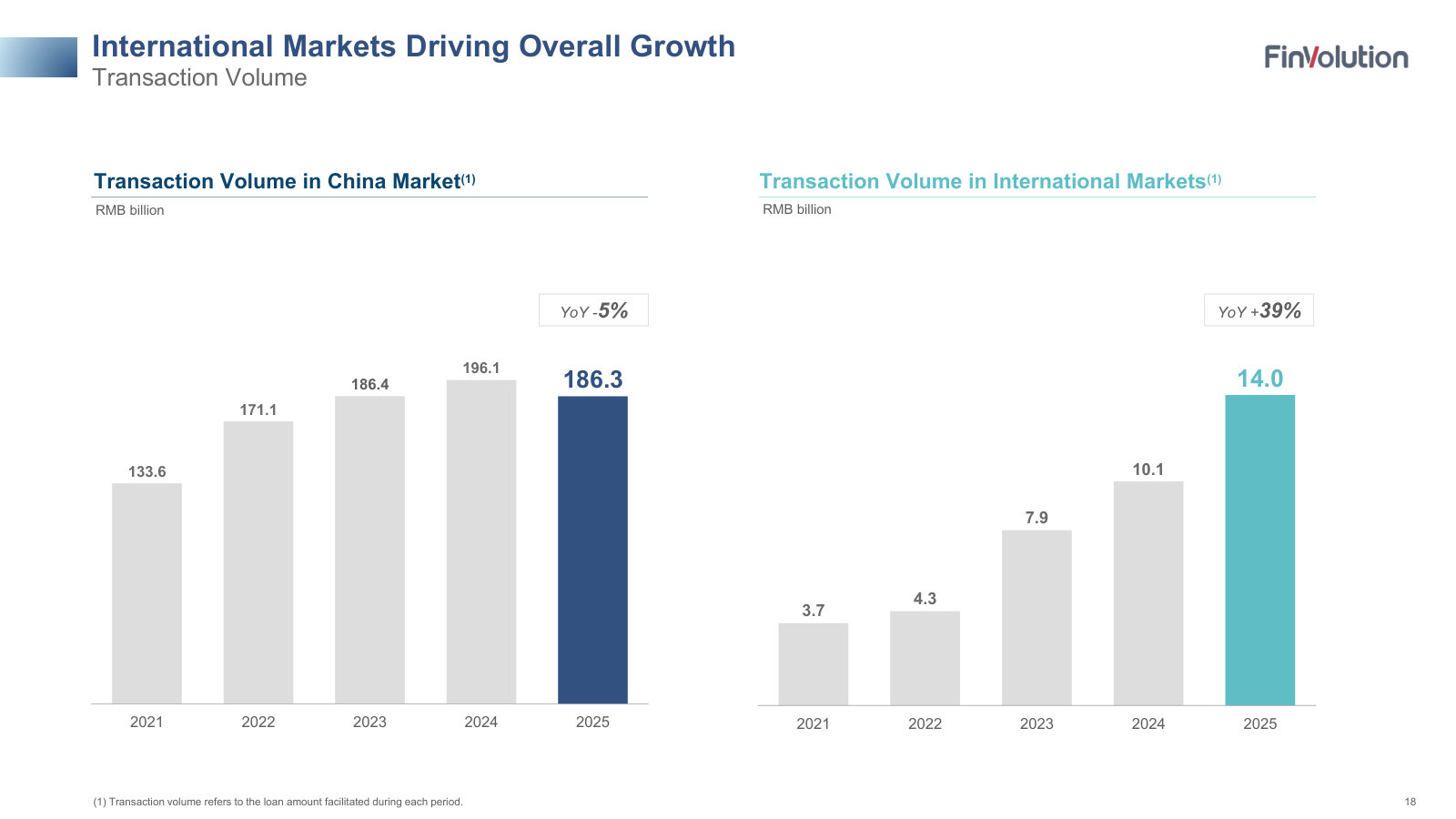

FinVolution facilitated ¥200.3 billion (US$28.6 billion) of loans in 2025 across roughly 240 million cumulative registered users, of whom 187.4 million are in China [8]. These are short-duration, small-ticket consumer loans: the China outstanding balance of ¥68.3 billion against ¥186.3 billion of annual origination implies the book turns over several times a year [9].

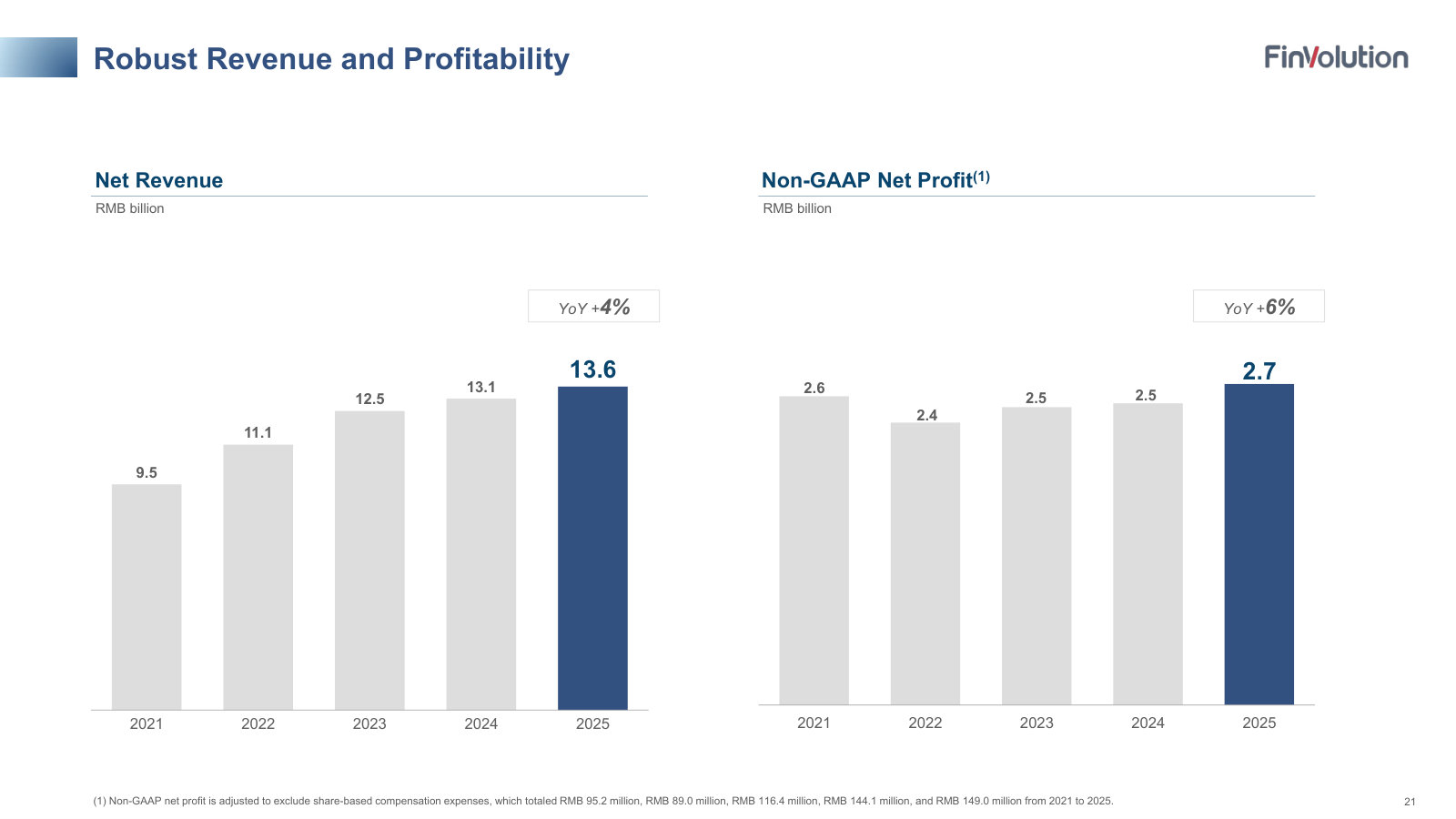

The revenue line has grown steadily; profit has not. Net revenue rose from ¥9.5 billion in 2021 to ¥13.6 billion in 2025 — up 43% — while net income attributable to shareholders was essentially flat, ¥2.51 billion then versus ¥2.54 billion now [10]. Net margin compressed from 26.5% to 18.7% over that span. The gap is the cost of the model: as FinVolution guarantees more of the loans it facilitates, credit provisions and guarantee costs absorb a rising share of each incremental revenue dollar — a dynamic later chapters will examine, and one a reader focused on cash-flow consistency should hold onto.

Source: FY2021–FY2025 Forms 20-F, Consolidated Statements of Comprehensive Income; latest year [11].

A maturing China book and a growing overseas one

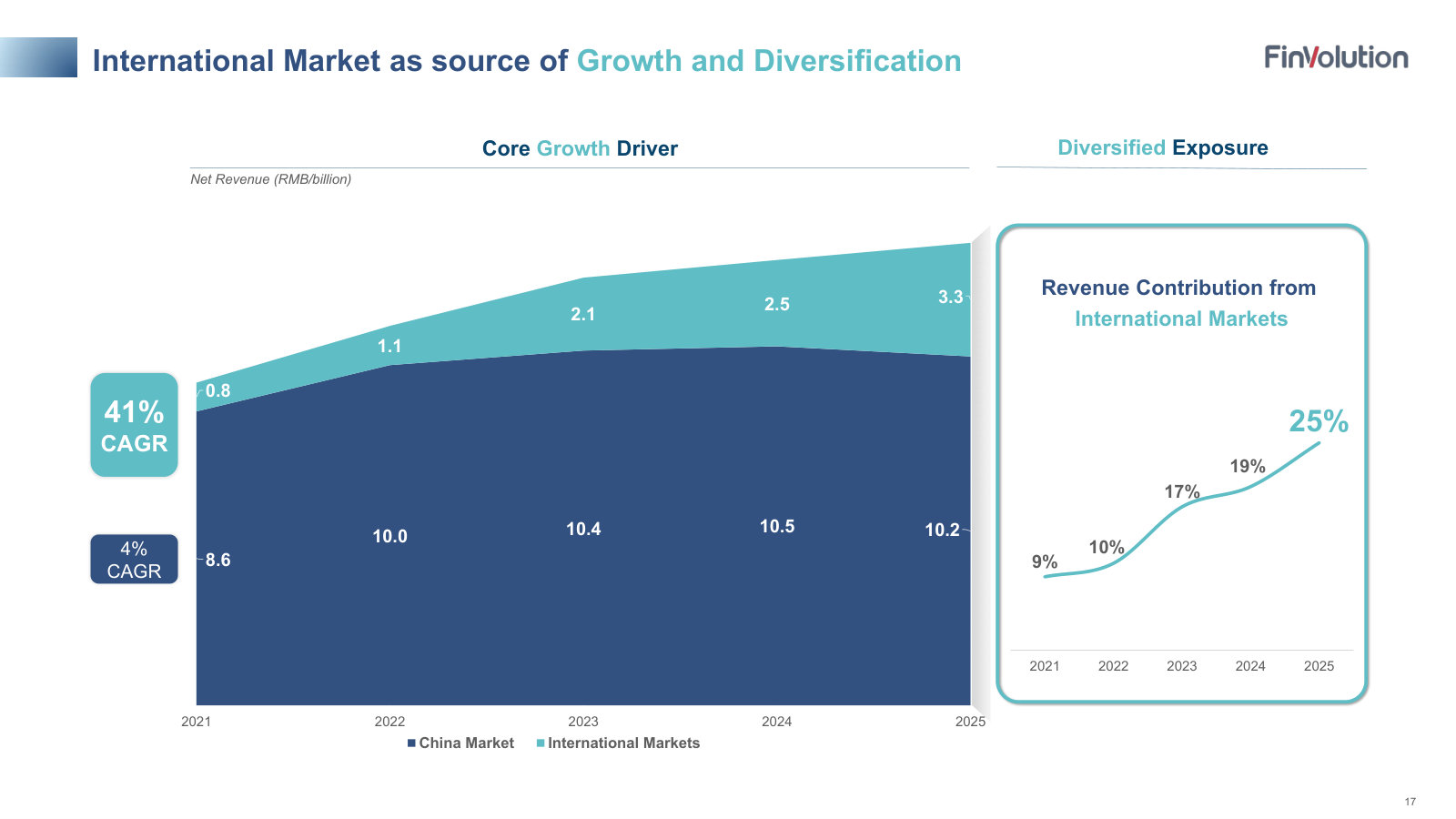

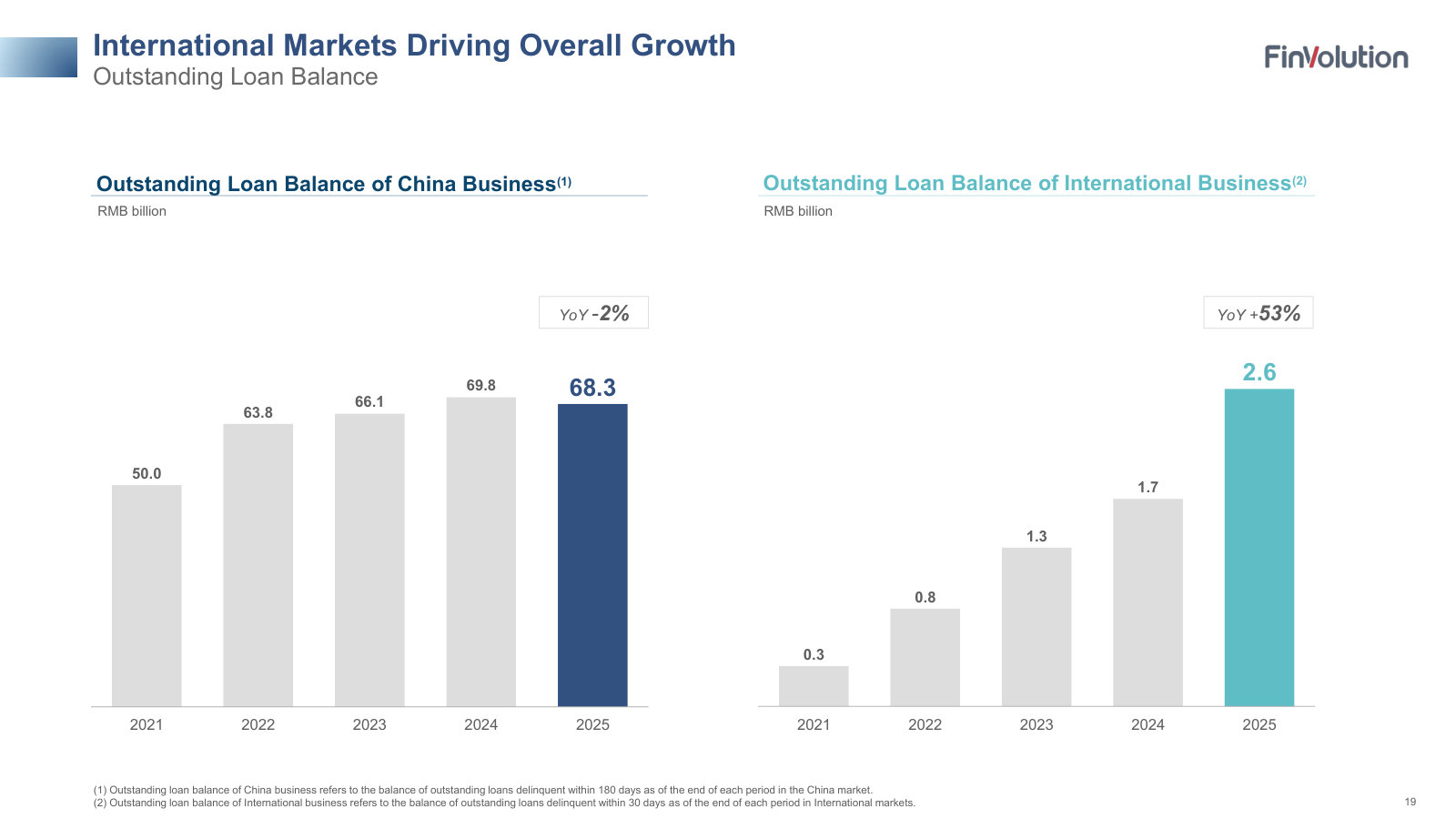

The composition of that revenue is where the operating story lives. China still supplies three-quarters of the total, but it is no longer growing: China revenue was ¥10.4 billion, ¥10.5 billion and ¥10.2 billion across 2023–2025, and China loan origination actually fell from ¥196.1 billion in 2024 to ¥186.3 billion in 2025 [12]. The overseas business is doing the growing: revenue from outside China rose from ¥2.14 billion to ¥3.33 billion (US$476 million) over the same three years, lifting its share of net revenue from 17.0% to 24.6% [13].

Source: FY2025 20-F, Item 4.B Business Overview [14].

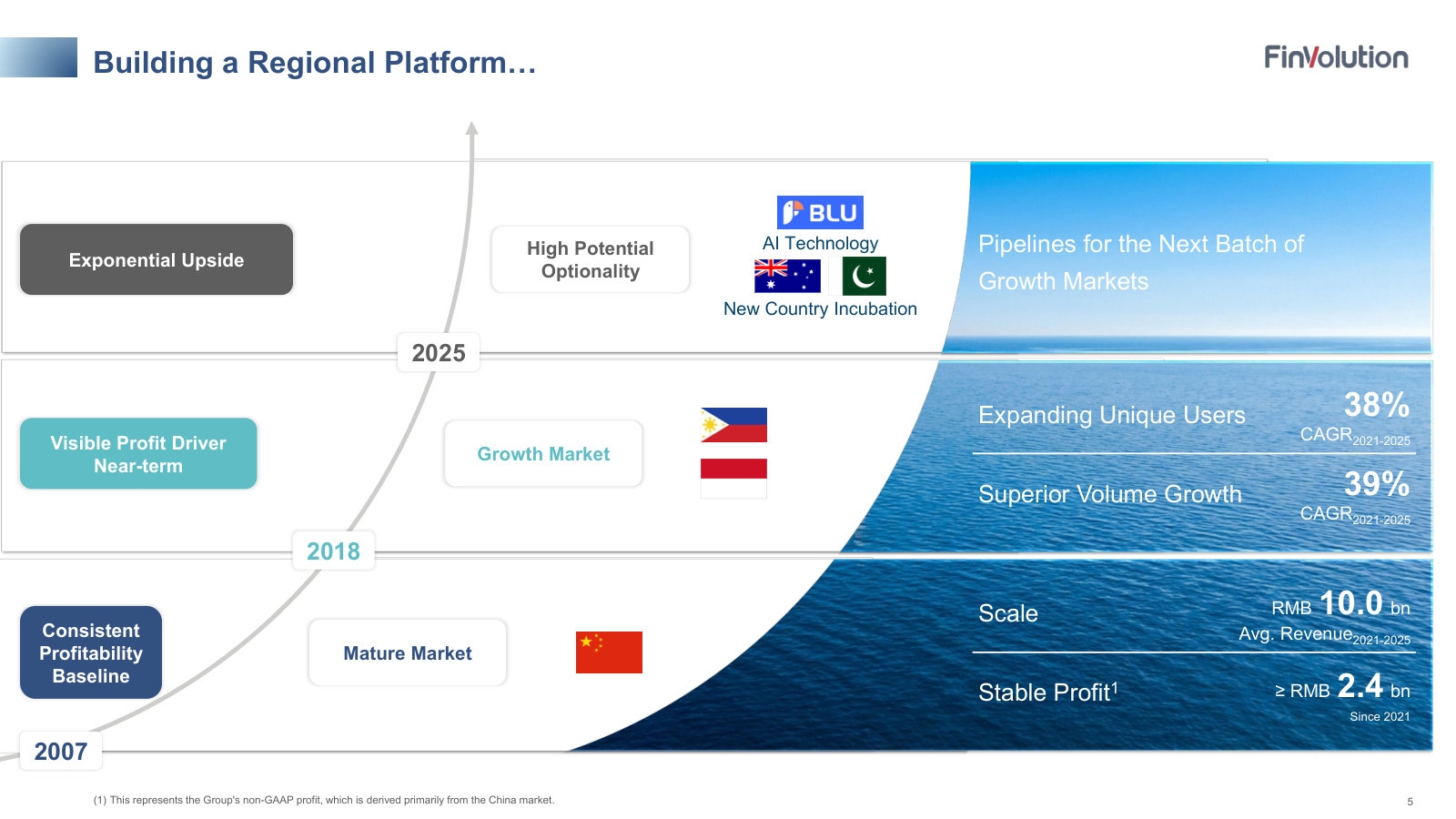

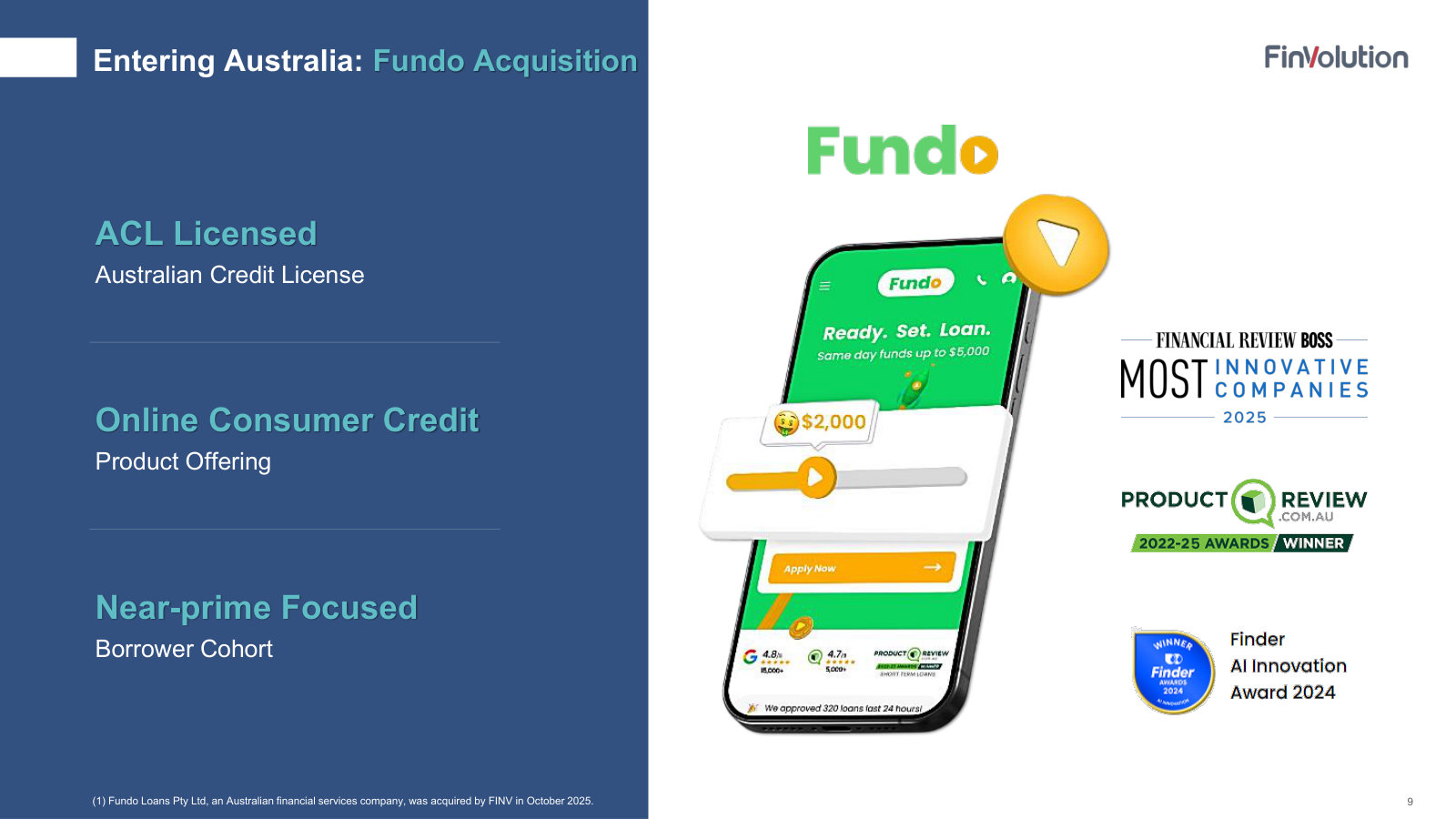

That overseas engine is built on markets FinVolution entered deliberately: Indonesia under the AdaKami brand in 2018, the Philippines under JuanHand in 2020, and — newest — Australia under the Fundo brand in October 2025, its first developed market [15]. Whether that engine is large enough, and profitable enough, to offset a flat China book is one of the questions the report will test; the overseas outstanding balance was still only ¥2.6 billion at year-end 2025, a fraction of China's ¥68.3 billion [16].

Credit quality is the counter-signal worth naming here. The 90-day-plus delinquency rate on the China book rose from 1.98% at the end of 2023 to 2.13% in 2024 and 2.85% in 2025 [17]. A rising delinquency rate on a shrinking domestic origination base is the fact a bull most has to explain, because FinVolution — not the funding bank — absorbs the loss on the majority of loans it guarantees.

The balance sheet and the discount

For a value-oriented reader, the balance sheet is the reason the low multiple is worth a second look rather than a reflexive pass. At the end of 2025 FinVolution held ¥4.29 billion of cash (US$613 million) and ¥3.02 billion of short-term investments (US$431 million) against modest borrowings and a single ¥1.0 billion convertible note — leaving roughly US$861 million of net cash, close to two-thirds of the company's market value [18]. Its only meaningful debt is US$150 million of 2.50% convertible senior notes due 2030, issued in June 2025 [19]. Shareholders' equity stood at ¥16.8 billion (US$2.41 billion) [20]. The board has declared a dividend every year and has steadily bought back stock, shrinking the share count from about 291 million to 267 million ADS-equivalents since 2022 [21].

Market cap (US$bn)

Trailing P/E (x)

Price / book (x)

Net cash (US$bn)

Source: derived from the FY2025 20-F Consolidated Balance Sheets and Statements of Comprehensive Income [22] [23], and NYSE market data.

At roughly US$4.78 per ADS, the market values FinVolution at about US$1.27 billion — some 3.5 times trailing net income of US$364 million, about 0.53 times book value, and barely above the company's net cash. Put differently, the market ascribes little value to a platform that facilitated US$28.6 billion of loans and generated US$364 million of profit last year.

The stock the market has marked down

Source: NYSE market data (FINV), as reported; year-end closing prices.

FinVolution priced its IPO at US$13 in November 2017. The shares more than halved within a year, bottomed near US$1.30 in 2020 as China's regulators dismantled the peer-to-peer lending model FinVolution was built on, and have since traded in a US$3–7 band without recovering the IPO price. Over the twelve months to July 2026 the ADS fell about 52%, from roughly US$10 to US$4.78, and now sits near its 52-week low — a decline steeper than any deterioration in the reported fundamentals, which is what makes the name a candidate worth the work rather than a simple falling knife.

The question this report examines

FinVolution presents a genuine contradiction: a business earning US$364 million a year, carrying net cash worth two-thirds of its market value and buying back its own stock, priced at 3.5 times earnings and below book. That price is not obviously wrong. The China loan book is flat and its delinquencies are rising; the fast-growing overseas business is still only a quarter of revenue; and the whole enterprise is a China-based consumer lender held through a VIE, exposed to PRC regulation and to the delisting and capital-transfer risks that discount every China ADR.

This report is built around one question: whether FinVolution's low-single-digit earnings multiple and below-book valuation are a durable margin of safety in a profitable, cash-generative platform, or a value trap in which a maturing China loan book with rising delinquencies, an overseas business still a quarter of revenue, and the regulatory and VIE overhang carried by every China ADR keep the discount permanently in place. The chapters that follow test the two sides of that question against the evidence — the economics of the guarantee model, the durability of the moat, the governance and ownership picture, the shape of the industry, and what the price implies.

The economics of the guarantee model

FinVolution's reported profit leans on an estimate. Guarantee income — 30% of 2025 net revenue — is the scheduled release of a liability the company books against its own forecast of loan losses, and it is nearly offset by the credit costs charged against the same loans. Reported profit converted to operating cash at about two-thirds over 2022–2025; the gap traces to a growing on-balance-sheet loan book and the working-capital intensity of the guarantee model, not to earnings that never arrive.

Figures are in renminbi (¥), FinVolution's reporting currency, with the company's own period-end US$ convenience translations from its Form 20-F where useful. Ratios and percentages are unitless. FX conversion tables were not supplied for this run, so a separate US-dollar edition is not produced.

What "guarantee income" actually is

For most of the loans it facilitates, FinVolution does not simply match a borrower to a bank and step aside. It stands behind the credit. Under its quality-assurance commitment, when a borrower funded by an institutional partner defaults, a guarantee company — third-party or one inside the group — repays the partner, and FinVolution is then obligated to reimburse that guarantee company for the same amount [1].

That promise creates two entries at the moment a loan is written, both governed by US accounting standards. One is deferred guarantee income, the fair value of the stand-ready obligation, released into revenue over time as the risk runs off [2]. The other is the liability from quality-assurance commitment, set at the expected lifetime credit losses of the covered loans — a figure derived from historical default experience, current conditions, and macroeconomic forecasts [3]. Guarantee income is the release of the first; the cost of the second flows through the income statement as credit losses. Both are management's estimates before they are anything else.

The mechanics are visible in the rollforward. The line "Release of quality-assurance obligations upon repayment" in the deferred-income schedule matches the "Guarantee income" line on the income statement to the thousand — ¥4,124.9 million in 2025 [4]. Behind that net figure sit gross flows an order of magnitude larger: the company paid out ¥7.7 billion to make partners whole in 2025 and recovered ¥4.3 billion from delinquent borrowers [5].

Source: FY2025 20-F, Note 2(s) deferred guarantee income and quality-assurance commitment rollforward [6].

Two balances are shrinking. Deferred guarantee income fell from ¥1,882 million at the end of 2023 to ¥1,119 million at the end of 2025, and the quality-assurance liability from ¥3,306 million to ¥2,575 million [7]. Management attributes the decline to a "decreased proportion of loans bearing credit risk in China," partly offset by more risk-bearing volume overseas [8]. The company is, deliberately, carrying less of its own China credit risk on its books than it used to.

The guarantee book is a thin, credit-sensitive layer

Guarantee income looks large — ¥4.1 billion, roughly 30% of net revenue — but it is not 30% of the profit. Set the guarantee income against the credit losses booked on the same commitment, and the net contribution is modest and volatile.

Source: FY2025 20-F, Consolidated Statements of Comprehensive Income — guarantee income and credit losses for quality-assurance commitment [9].

In 2023 the guarantee book was essentially breakeven: ¥4,479.0 million of income against ¥4,422.8 million of credit losses, a net ¥56 million [10]. By 2025 it earned ¥663 million as losses fell faster than income — about a fifth of the ¥3,101 million pretax profit [11]. Widen the lens to all credit costs — the quality-assurance losses plus provisions for loans receivable and for accounts receivable — and total credit charges of ¥4,526 million in 2025 exceeded guarantee income of ¥4,125 million [12].

The profit engine, then, is fees, not the guarantee. Loan-facilitation and post-facilitation service fees together were ¥6,806 million in 2025, with net interest income of ¥1,336 million; the guarantee layer sits on top as a small, swing contribution whose sign depends on how well the loss estimate holds [13]. That is why the group's net margin compressed even as revenue grew — the same dynamic the Business and Discount chapter flagged: rising credit charges absorb an outsized share of each incremental revenue dollar.

Profit converts to cash at about two-thirds

For a lender that guarantees its book, the more important test is whether the estimated profit shows up as cash. Over the last four years it has, partially. Operating cash flow trailed net profit in three of four years, and equaled it in none but 2024.

Sources: net profit, FY2025 20-F Statements of Comprehensive Income [14] and FY2022 20-F [15]; operating cash flow, FY2025 20-F cash-flow summary [16] (2022 figure restated per note below).

Cumulatively, FinVolution generated ¥6.36 billion of operating cash on ¥9.60 billion of net profit across 2022–2025 — a 66% conversion rate. The single weakest year, 2022, converted just 10% [17]. Three structural gaps explain most of the shortfall, and none of them is a sign that the profit is fictional.

First, a large slice of revenue is non-cash at the operating line. "Net interest income" earned on loans FinVolution originates and holds itself — through consolidated trusts and its overseas books — is recognized as a "net gain from investment in loans" and then removed from operating cash flow, because the actual cash for those loans is classified as investing activity. That reversal was ¥1,336 million in 2025 [18]. The company deployed ¥18.4 billion into these loans and collected ¥16.8 billion back during the year — real cash generation that never touches the operating-cash line [19]. As this on-balance-sheet book grows, reported operating cash understates the group's economic cash flow.

Second, the guarantee model is working-capital intensive. Growth requires posting security deposits with funding partners and building quality-assurance receivables, both of which consume cash as volume expands. In 2022 that drag was acute: a ¥914 million build in quality-assurance receivable and a ¥1,153 million increase in prepaid expenses and other assets — chiefly security deposits — pulled operating cash down toward zero even as profit held near ¥2.3 billion [20]. When that cycle reverses, as it did in 2024, operating cash can exceed profit — a ¥1.7 billion release from prepaid assets drove the 121% conversion that year [21].

Third, the timing of the guarantee accruals themselves — releases of deferred guarantee income and changes in the quality-assurance liability — and rising deferred-tax assets move the operating line year to year without changing the underlying economics [22].

One point on comparability: in the fourth quarter of 2024 FinVolution reclassified certain customer-funds flows between financing and investing activities and restated prior years, which is why 2022 operating cash appears as ¥236.9 million in the latest filing versus ¥268.8 million as originally reported [23]. The change did not touch the profit-to-operating-cash relationship, and the operating figures shown above are on the restated basis.

That the profit is cash-taxed is a useful check against the worry that it is an accounting mirage: FinVolution paid ¥963 million of income tax in cash in 2022, more than double its book tax expense that year, as earlier deferrals unwound [24].

Where the estimate gets tested

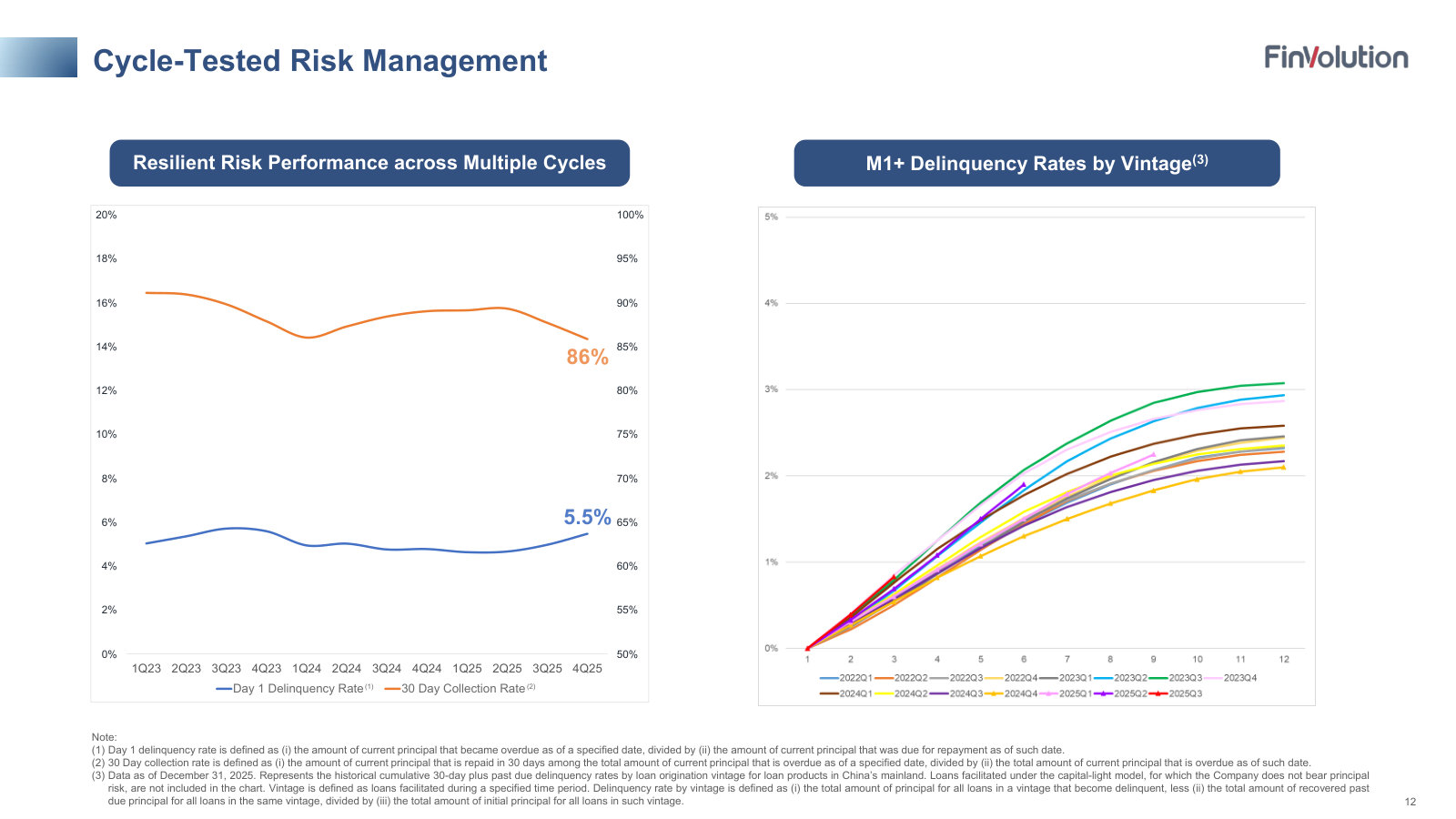

The durability of this profit rests on whether the loss estimate embedded in the guarantee liability proves right. That estimate is now being pressed. The 90-day-plus delinquency rate on FinVolution's China book rose from 1.98% at the end of 2023 to 2.13% a year later and 2.85% at the end of 2025 — a 44% increase in the delinquency ratio over two years [25].

Source: FY2025 20-F, Loan Performance Data — 90 Day+ Delinquency Rate [26].

Because guarantee income is fixed at the loan's inception while credit losses accrue against actual performance, worsening delinquency squeezes the guarantee book's thin margin first and the group's reported profit next — the mechanism behind the multi-year margin compression. This is the point on which the durable-versus-trap question turns from the cash-quality side: if realized losses run above the reserved estimate, provisions rise and profit falls; if the estimate proves conservative, the reverse.

Two facts weigh against reading the rising delinquency as an unmanaged deterioration. Management has publicly tightened underwriting — cutting exposure to lower-quality acquisition channels, trimming credit limits for higher-debt borrowers, and deploying earlier-stage AI collection — and has built a reserve buffer: it disclosed a provision-coverage ratio of 543% in the second quarter of 2025, up from 465% a quarter earlier [27]. And the ¥4.3 billion of gross recoveries collected in 2025 shows the collection machinery behind the estimate is real, not notional [28].

The read that fits the evidence: FinVolution's profit is real and cash-taxed, but it is estimate-dependent and credit-sensitive in a way a fee-only platform's is not, and it converts to operating cash at roughly two-thirds because the model funds its own growth in working capital and on-balance-sheet loans. What would change the read is the delinquency trend against the reserve: a coverage ratio that holds or rises while losses stay inside the reserved estimate would confirm the profit is durable; a coverage ratio that falls as delinquency climbs would mark the estimate — and the profit built on it — as too optimistic.

Who owns FinVolution, and who controls it

The people who run FinVolution also own it and control it. The four co-founders and the management team hold 53.6% of the shares and 91.2% of the votes; chairman Shaofeng Gu alone commands 66.4% of the vote on 36.4% of the economics, through shares that carry twenty votes each. That concentration is one reason a profitable, net-cash company trades where it does — an outside shareholder has no path to force a change. It comes paired with unusually high alignment: the same insiders return cash through dividends and buybacks and bought more stock as it fell.

Ownership figures are as of March 31, 2026, from the FY2025 Form 20-F. Financial figures are in renminbi (¥), FinVolution's reporting currency, with the company's own period-end US$ convenience translations where useful; the ADS trades on the NYSE in US dollars, so dividends, buyback prices, and share value are shown in dollars. Percentages are unitless. FX conversion tables were not supplied for this run, so a separate US-dollar edition is not produced.

The control snapshot

Insiders' economic stake

Insiders' voting power

Chairman Gu's voting power

Public ADS voting power

Source: FY2025 Annual Report (Form 20-F), Item 6.E Share Ownership [1]; Item 3 Key Information [2].

FinVolution runs a dual-class structure. Class A ordinary shares — the shares underlying the NYSE-listed ADSs — carry one vote; Class B ordinary shares carry twenty votes each and are convertible one-for-one into Class A at the holder's option, while Class A can never convert to Class B [3]. All 566.7 million Class B shares sit with the four co-founders and management. As a result the Class B block held 94.9% of the company's aggregate voting power at March 31, 2026, and a single holder — chairman and chief innovation officer Shaofeng Gu — controlled 66.4% of the vote [4]. An ADS holder buys the cash flows; the founders keep the company.

The ownership table

Source: FY2025 Annual Report (Form 20-F), Item 6.E Share Ownership, based on 1,180.5 million ordinary shares outstanding (613.8m Class A, 566.7m Class B) at March 31, 2026 [5] [6].

Three features stand out. First, control does not sit with the operating CEO. Tiezheng Li, the chief executive, holds 4.8% of the vote; Gu, who chairs the board and carries the chief-innovation-officer title, holds 66.4% [7]. Whoever runs the business day to day, the last word rests with the chairman. Second, the founders' economic interest is large and real: at 53.6% of the shares, roughly half of every renminbi of profit and every dollar of buyback accrues to them alongside outside holders — the incentive to grow per-share value is their own. Third, outside ownership is thin and passive: the largest non-insider holder disclosed, the Susquehanna entities, holds 7.0% of the shares but 0.7% of the votes [8].

The buyback quietly tightens the founders' grip

The share count has been shrinking, and it shrinks in one direction only. Between March 2025 and March 2026 the Class A count fell from 700.4 million to 613.8 million — a 12.4% reduction of the public class in a single year — while the 566.7 million Class B shares held by insiders did not move [9] [10]. Buybacks retire only Class A. So each repurchase mechanically lifts the founders' share of both economics and votes without their spending a cent.

Source: FY2021–FY2025 Forms 20-F, Item 6.E Share Ownership tables [11] [12] [13] [14] [15].

The insiders' economic stake climbed from 44.0% in 2022 to 53.6% in 2026, and Gu's voting power from 63.7% to 66.4%, with little open-market buying behind the move — the float did the work. This is the double edge of a shareholder-friendly capital return under a dual-class charter. The buyback that returns cash to Class A holders also, year by year, concentrates the company further in the founders' hands. For a minority holder the practical consequence is blunt: the discount will not be closed by a proxy fight, an activist, or a takeover, because none is possible against 91% of the vote.

What the controllers do with the cash

The offsetting fact is what those controllers have chosen to do with the company's surplus. FinVolution behaves like a business run by owners who want cash out, not empire-builders.

2026 dividend per ADS ($)

Buybacks deployed, 2 programs ($M)

Insider open-market buying, 2025 ($M)

Source: FY2025 Annual Report (Form 20-F), Item 8.A Dividend Policy and Item 16E Purchases of Equity Securities [16] [17].

The board has declared a dividend every March from 2019 through 2026, and in March 2025 it formalized a policy to distribute 20% to 30% of the prior year's net income each year; the March 2026 dividend was set at $0.306 per ADS [18]. Cash dividends paid to U.S. investors rose from ¥416.5 million in 2023 to ¥510.2 million (about $73.0 million) in 2025 [19].

On top of the dividend sit two $150 million buyback authorizations — a 2023 program that retired about 27.3 million ADSs, and a 2025 program that had bought a further 18.8 million ADSs at an average $6.22 by March 2026, roughly $267 million deployed across the two [20] [21]. The pace tells its own story: as the ADS fell from about $9.50 in mid-2025 toward $5.20 by early 2026, the company bought more, not less.

Source: FY2025 Annual Report (Form 20-F), Item 16E — monthly repurchases under the 2025 Share Repurchase Program [22].

Management also put its own money in alongside: members of senior management bought approximately $1.9 million of ADSs in the open market during 2025, outside the company's programs [23]. And the take is modest at the top: FinVolution paid its directors and officers as a group about ¥27.0 million ($3.9 million) in cash for 2025 — roughly 1% of net income — with no pension or retirement accruals [24]. A controlling family paying itself little, buying stock personally, and shrinking the float into weakness is the behavior of owners compounding value, not extracting it.

The related-party channel — small, so far

Concentrated control is a standing invitation to self-dealing, so the related-party record is worth checking directly. Two channels exist. The first is structural: FinVolution consolidates its Chinese operations through variable-interest entities whose equity is registered not to the listed company but to the four co-founders and a few of their family relatives, backed by call options and interest-free loans of ¥100 million that fund the nominees' capital contributions [25] [26]. The nominees being the controlling founders cuts both ways: it removes the risk of an unaffiliated nominee going rogue, but it concentrates the VIE conflict in the same hands that already hold the votes, and the company states plainly it cannot assure that these shareholders will resolve conflicts in its favor [27].

The second channel is operating transactions, and here the disclosed amounts are small. At the end of 2025, amounts due to related parties totaled ¥18.7 million and amounts due from them ¥36.7 million; the largest recurring item was ¥29.9 million of operation-and-support-services expense to Smart Frontier, an equity-method investee [28]. A founder-owned data provider, PPcredit, supplies data at prices the company says are set by reference to other market participants [29]. Against ¥13.6 billion of revenue these figures are rounding error — under 0.3% of the top line. On the evidence in the filings, the control has not been used to route cash to insiders; the cash has gone out as dividends and buybacks instead.

The guardrails a minority holder actually has

They are few, and they are largely self-imposed. As a Cayman Islands company and a foreign private issuer, FinVolution follows home-country practice and is exempt from the NYSE rules that would otherwise require a majority-independent board, a fully independent compensation committee, and an annual shareholders' meeting; it does not hold one [30]. Its directors, officers, and principal shareholders are also exempt from the Section 16 insider-reporting and short-swing-profit rules that apply to domestic issuers [31]. The board is seven directors, three of them independent — a minority, not a majority; the chair (Gu) and CEO (Li) titles are split, but both are co-founders, so the separation is organizational rather than a genuine independent check [32].

The read that fits the evidence: FinVolution scores poorly on governance rights and well on governance behavior. A minority ADS holder owns cash flows over which they have no vote and no exit lever, under a charter that entrenches the founders a little more with every buyback. What protects that holder is not structure but conduct — a controlling family whose own 53.6% stake ties its wealth to the same per-share value, and whose revealed pattern is aggressive, price-sensitive cash return rather than extraction. The counter-case is that the record is only a record: nothing in the structure prevents a future pivot to dilutive deals, Class B issuance, or larger related-party flows, and outside holders would have no means to stop it. The check to watch is therefore behavioral — whether related-party balances stay immaterial, whether buybacks and the 20%–30% payout continue, and whether insiders keep buying rather than selling. So long as those hold, the concentration reads as aligned control; if they break, the same concentration becomes the mechanism of a value trap.

Overseas Engine

FinVolution now runs two businesses with opposite trajectories. The China platform is a maturing, high-margin book in managed decline; the overseas platform — Indonesia, the Philippines and, since October 2025, Australia — is growing fast and, as of the first quarter of 2026, is disclosed as a separate reportable segment for the first time. That disclosure settles a question earlier chapters could only flag: overseas is 29.6% of revenue but earns a 4.8% operating margin against China's 27%, so it adds tens of millions of profit while China sheds hundreds.

The revenue map has tilted toward Asia beyond China

Geographic disclosure begins in FY2021, and the shift since is steady rather than sudden. Revenue from outside the Chinese mainland rose from about RMB0.83 billion in 2021 to RMB3.33 billion in 2025 — from 8.7% of the group to 24.6% — while China revenue was essentially flat across the five years and dipped in 2025 [1] [2].

Source: FY2025 Form 20-F, Note 22 Geographic information (2023–2025) [3]; FY2023 Form 20-F for 2021–2022 [4]. Overseas = total less the PRC.

By 2025 the two components were pulling apart on volume as well as revenue. Full-year loans facilitated in international markets reached RMB14.0 billion, up 38.6%, while China volume fell 5.0% to RMB186.3 billion and the group total slipped 2.9% to RMB200.3 billion [5]. Within the overseas total, the Philippines is the fastest riser — revenue there grew from RMB0.25 billion in 2023 to RMB1.19 billion in 2025 — with Indonesia the larger but slower base at RMB2.04 billion [6].

Two segments, two margins

The first-quarter 2026 release is the inflection in disclosure. Management began "reporting our overseas business as a separate reportable segment," and the segment table puts hard numbers on a gap that was previously only inferable [7]. Overseas earned RMB948.9 million of net revenue — 29.6% of the group — but only RMB45.8 million of segment operating profit. China earned RMB598.7 million of operating profit on RMB2,216.1 million of revenue [8].

Source: derived from Q1 2026 Selected Segment Information (China margin = RMB598.7m / RMB2,216.1m; overseas = RMB45.8m / RMB948.9m; prior-year comparatives recast) [9].

The direction of travel inside each engine matters as much as the levels. Overseas operating profit rose 87.7% year on year, from RMB24.4 million to RMB45.8 million, and its margin widened from 3.5% to 4.8% [10]. Over the same quarter China's operating profit fell 34.4%, from RMB913.1 million to RMB598.7 million, as tighter underwriting cut volume 21.6% [11] [12]. The arithmetic of the "two-engine" framing is unforgiving on current numbers: the overseas engine added about RMB21 million of operating profit while the China engine gave back about RMB314 million, so group operating profit fell 38% to RMB546.8 million and net profit fell to RMB421.1 million from RMB737.6 million a year earlier [13].

Overseas share of revenue

Overseas share of operating profit

Overseas operating margin

Source: Q1 2026 Selected Segment Information; overseas operating profit RMB45.8m is 8.4% of group operating profit RMB546.8m [14].

High yield paid for with high cost

The overseas book carries a much higher revenue take per unit of lending. Across full-year 2025, international revenue of RMB3.33 billion on RMB14.0 billion of volume implies roughly RMB0.24 of revenue for every RMB1 originated; the China book generated RMB10.24 billion on RMB186.3 billion, closer to RMB0.055 [15] [16]. Two things drive the roughly four-fold gap, and both cut against reading it as pure margin. Overseas loans are short and high-rate — the Indonesia book runs a three-to-four-month tenor, so the same principal is re-lent several times a year and each cycle books fee revenue [17]. And a large part of China volume now passes through a capital-light model that carries no principal risk and a thinner take — RMB15.5 billion of the first quarter's China volume [18].

The high revenue yield does not survive to the operating line because acquiring and collecting from overseas borrowers is expensive and the base is still being built. Overseas unique borrowers more than doubled year on year in the first quarter, to 4.5 million, and cumulative overseas borrowers reached 13.4 million, up 76.3% [19] [20]. Growth that fast means heavy user-acquisition and collection spend landing ahead of the revenue it eventually earns, which is why the segment converts a 24%-of-volume revenue yield into a mid-single-digit operating margin. The margin has moved the right way — 3.5% to 4.8% in a year — but it has a long way to climb before it resembles the mature China book.

Where the regulation is heading

The economics that make overseas lending lucrative are the same ones regulators across the region are compressing, and this is the central risk to the growth case. In Indonesia, the OJK set a schedule to cut the daily interest-rate cap on consumptive fintech loans from 0.4% in 2023 toward 0.1% by 2026; at the end of 2024 it replaced the uniform cut with tenor-based caps — 0.3% for loans of six months or less, 0.2% above that [21]. Because AdaKami's loans sit inside the six-month band, that revision is a reprieve rather than a cut to 0.1%. The Philippines moved the other way: a securities-regulator memorandum effective April 1, 2026 imposes a 12% monthly cap on effective rates for small loans up to PHP 10,000 [22]. And enforcement is live, not theoretical — in March 2026 Indonesia's antitrust agency fined 97 online lenders for alleged rate coordination, with AdaKami assessed IDR 102.3 billion, about RMB 41.7 million, now under appeal [23].

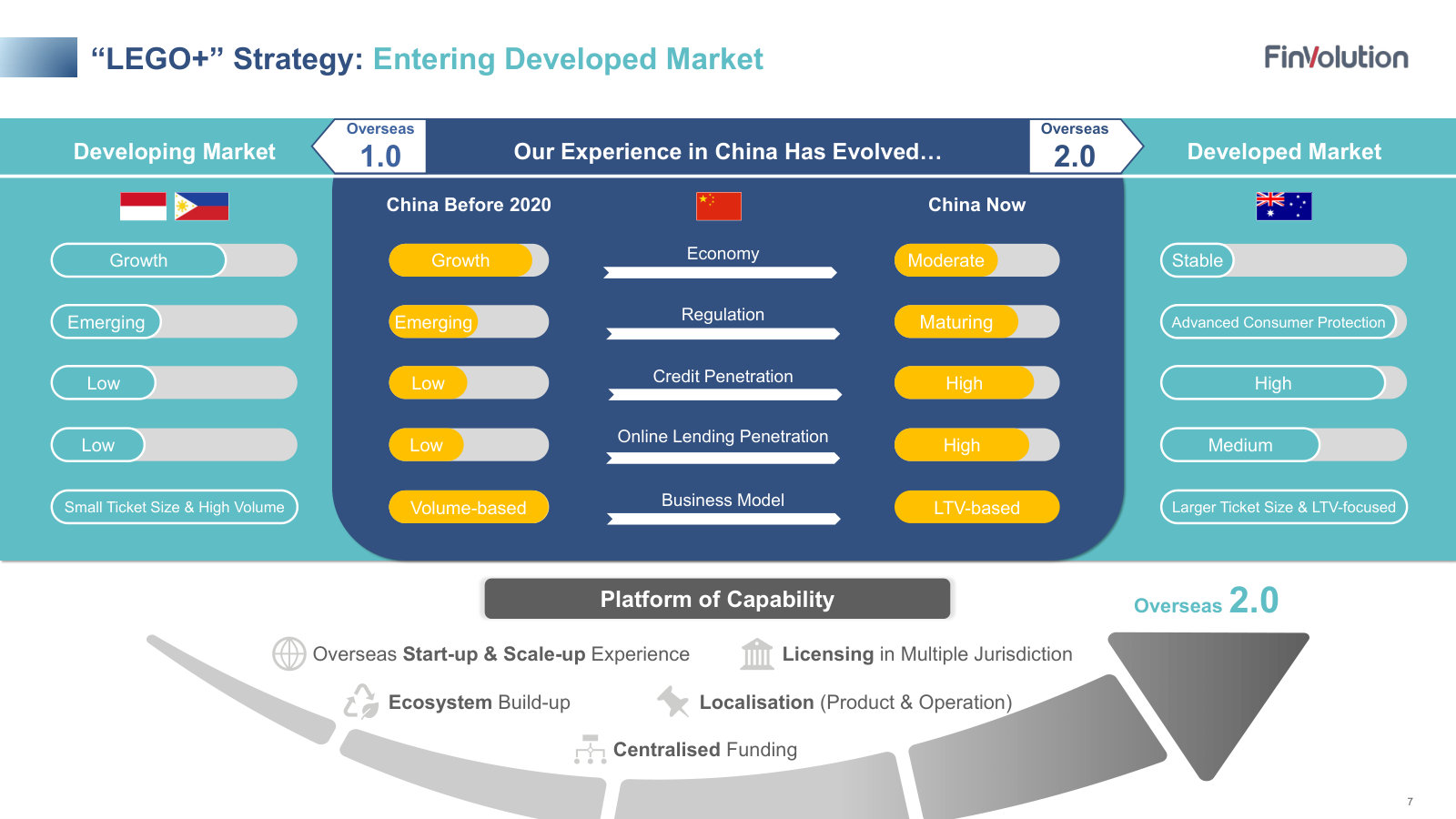

The Australia entry reads as a deliberate answer to that pressure. FinVolution stepped into its first developed market by acquiring Fundo — 40% for AUD 16.0 million in July 2025, then the remaining 60% for AUD 33.1 million in October 2025 — a holder of an Australian Credit Licence lending to near-prime borrowers [24] [25]. A developed market carries a higher entry barrier and, management argues, more stable rules and larger, longer-dated loans than the volume-driven emerging-market model [26]. It is early — Australia sits in the "Others" line that lost money at the segment level in the first quarter — but it signals where management thinks durable overseas profit comes from.

On the China side, management's own framing is that the domestic market is mature and being run for quality rather than growth. On the third-quarter 2025 call the CEO described eighteen years spent navigating the P2P-to-facilitation transition and "several interest rate cap adjustments," and said the company had "decisively prioritized quality over quantity," raising underwriting standards and cutting sales-and-marketing spend 12% quarter on quarter [27]. The same call characterised the overseas platform as "one of the few scaled overseas platforms in our sector" [28]. That head start is real relative to peers — Chinese competitor Yiren Digital only launched its Indonesian operations in September 2025 [29] — and FinVolution reports full-year 2025 profitability in both Indonesia and the Philippines [30].

What it means for the growth half of the case

The overseas engine is genuinely scaling, now separately profitable, and improving its operating leverage — the bull evidence is the 87.7% jump in overseas operating profit and the margin moving from 3.5% to 4.8% in a year [31]. The counter is that it remains too small in profit terms to offset China's decline: overseas is 29.6% of revenue but only about 8% of operating profit, and in the latest quarter its growth replaced barely a fifteenth of the profit China gave up [32]. Full-year 2025 still showed group net profit up 6.6% to RMB2.5 billion, but the fourth-quarter and first-quarter run-rate — net profit down to RMB415.5 million then RMB421.1 million — shows the China drag reaching the bottom line [33] [34].

For the growth half of the durable-versus-trap question, the swing factor is overseas operating margin, not overseas revenue. Revenue growth is already established; what is unproven is whether a mid-single-digit margin can climb toward the China book's mid-twenties as the borrower base matures and acquisition spend normalises — and whether it can do so while Indonesian and Philippine rate caps tighten. The read that would change is a second and third quarter of overseas margin expansion that outpaces the China profit decline; the read that would harden the value-trap case is overseas margin stalling near 5% while regulation caps the yield that funds it.

The segment split now makes both readable in real time. The line to watch is the overseas operating margin in the quarterly Selected Segment Information, against the pace of the China operating-profit decline in the same table.

Competitive Position

FinVolution is a strong operator in a business with weak barriers. Set against six listed Chinese loan-facilitation peers, it is the second most profitable of the group, but its take rate, credit performance and funding are middle-of-the-pack — nothing structural separates it from rivals in its China core, where the largest peer, Qifu, earns 2.4 times its profit at a comparable loss rate. Its one durable, hard-to-copy advantage sits offshore: a multi-year overseas head start no peer has matched. On the evidence, a narrow moat.

The peer set

All six comparables run a recognisably similar model: a Cayman-listed platform that matches Chinese consumer borrowers to licensed institutional funders (banks, consumer-finance companies, trusts), takes a fee, and carries some of the credit risk through a guarantee. That shared structure is why the group is a fair mirror — and why size, not model, is what separates them.

*Lufax figures FY2025; it ran a net loss, so ROE is not meaningful and its take rate is not comparable (it is a small-business-owner and secured lender, larger-ticket than FINV's consumer micro-loans). **Lexin figures are FY2024 (its latest 20-F); all others FY2025. ROE = net income ÷ year-end shareholders' equity. Sources: FINV FY2025 20-F [1], [2], [3]; QFIN FY2025 20-F [4], [5], [6]; Lufax FY2025 20-F [7]; Lexin FY2024 20-F [8], [9], [10]; X Financial FY2025 20-F [11], [12], [13]; Jiayin FY2025 20-F [14], [15], [16]; Yiren FY2025 20-F [17], [18], [19].

Qifu is the scale leader by a distance: RMB327.1 billion of loan volume against FinVolution's RMB200.3 billion, and RMB5.99 billion of net income — 2.4 times FinVolution's RMB2.54 billion [20][21]. Below Qifu, FinVolution is the most profitable name in the group: its RMB2.54 billion tops Jiayin (RMB1.54 billion), X Financial (RMB1.46 billion), Lexin (RMB1.10 billion) and Yiren (RMB0.05 billion), and stands against a RMB1.70 billion loss at the larger Lufax [22][23][24]. That places FinVolution as a solid second — profitable, mid-scale, but not the operator others must react to.

Net income attributable to shareholders; latest fiscal year (FY2025 except Lexin FY2024). Sources as in the table above: FINV [25]; QFIN [26]; JFIN [27]; XYF [28]; LX [29]; YRD [30]; LU [31].

No structural edge in China

A moat should show up in numbers — in pricing, in credit, or in a funding cost rivals cannot match. On each of those tests FinVolution reads as competent rather than advantaged.

Pricing. Expressed as net revenue over loan volume — a rough take rate — the comparable consumer lenders cluster in a narrow band. FinVolution's 6.8% sits at the top of that band, but only just above Lexin's 6.7% and within a point of Qifu's and X Financial's 5.9%.

Derived from each company's reported net revenue and loan volume (latest fiscal year; Lexin FY2024). †Yiren's figure is flattered by non-lending revenue — roughly an eighth of its total comes from insurance brokerage and lifestyle services rather than loan facilitation. Lufax excluded (different, larger-ticket model). Sources: net-revenue and volume citations as in the peer table — FINV [32][33]; QFIN [34][35]; LX [36][37]; XYF [38][39]; JFIN [40][41]; YRD [42][43].

The narrow spread is what commoditised pricing looks like: rates are set less by any platform's brand than by the regulatory ceiling all of them face and the returns institutional funders demand. A clean loan-facilitation take rate near 7% is respectable, not a source of advantage.

Credit. On the closest like-for-like measure — the point-in-time 90-day-plus delinquency rate on the outstanding book — FinVolution again sits in the middle. Its China book ran at 2.85% at end-2025, just above Qifu's 2.71% and below Lufax's 3.4% and Lexin's 3.6% [44][45][46][47]. The remaining three report on bases that do not line up cleanly — Jiayin discloses a vintage-based M3+ rate rather than a book delinquency rate [48], and X Financial's disclosed buckets deteriorated sharply, its 91-to-180-day delinquency rate climbing to 6.31% at end-2025 from 2.48% a year earlier [49]. The read across the group is that credit is cyclically softening for everyone; FinVolution is managing it as well as the best and better than the weakest, but its underwriting is not visibly a class apart.

Funding. Every platform draws on the same pool of licensed lenders, on non-exclusive terms. FinVolution had cumulatively worked with 115 institutional funding partners in China as of end-2025 [50]; the same banks, consumer-finance companies and trusts fund its rivals, and no single partner is committed to any one platform. That is a shared, contestable input, not a proprietary one — which is why the whole group also carries credit risk on the loans it places, FinVolution included, rather than earning a pure risk-free fee [51].

The China lending economics are examined in Guarantee Economics; the point here is comparative. Nothing in pricing, credit or funding gives FinVolution an edge a well-run rival lacks. In its home market it is a good operator in a crowded, rate-capped business — which is closer to execution than to a moat.

The overseas head start

The one place the peer comparison genuinely separates FinVolution is offshore. It has built a scaled international business while the rest of the group has barely started.

Intl loan volume FY2025 (RMB bn)

Overseas share of revenue

Overseas unique borrowers (m)

FinVolution FY2025: international loan origination RMB14.0 billion (up from RMB7.9 billion in 2023), 24.6% of revenue, 5.9 million overseas unique borrowers, funded through 18 overseas institutional partners. Source: FY2025 20-F [52]; overseas revenue share per Overseas Engine.

Against that, the peer field is thin. Qifu began overseas expansion only in 2024, extending into "several overseas markets" with no overseas scale disclosed [53]. Jiayin opened an Indonesia office back in 2019 but has since disposed of its Nigeria operations and shows little overseas volume [54]. Yiren is the earliest of the followers into FinVolution's own markets, but frames the Philippines and Indonesia as businesses to "gradually expand" from a small base [55]. Lexin and X Financial were China-only in their latest filings.

Sources: FINV FY2025 20-F [56]; YRD Q4 FY2025 transcript [57]; QFIN FY2025 20-F [58]; JFIN FY2025 20-F [59]; LX FY2024 20-F [60]; XYF FY2025 20-F [61]; LU FY2025 20-F [62].

This lead is harder to copy than a China take rate. It rests on things that take years to assemble in each market: local lending licences, a repeat-borrower base (87.6% of overseas volume in 2025 came from returning borrowers), and underwriting data on populations with little formal credit history [63]. A peer entering Indonesia today starts where FinVolution stood several years and 18 funding relationships ago.

A narrow moat

The evidence points to a narrow moat. FinVolution has no structural advantage in its China core — it prices, underwrites and funds much like its rivals, and a larger peer out-earns it while reserving as conservatively. What it does have is a scaled, hard-to-replicate overseas franchise that every competitor is years behind on, and a second-place profit standing that says it executes well.

The strongest fact against calling even that a moat is size and quality of earnings. The overseas franchise, for all its lead, is still under a quarter of revenue and earns a mid-single-digit operating margin against China's high-twenties, so the durable edge is real but does not yet carry the group's profitability — the detail is in Overseas Engine. A first-mover position that does not yet earn first-mover economics is a narrow moat, not a wide one.

What would change the read in either direction is observable. Widen it: overseas operating margins converging toward China's as the borrower base seasons, which would turn a revenue lead into a profit moat. Narrow it: Yiren, Qifu or a fresh entrant reaching real scale in Indonesia or the Philippines within a few years, which would show the head start was a timing advantage rather than a barrier. Both are checkable in the segment disclosures from here.

What US$4.78 buys

At about US$4.78 per ADS FinVolution is worth roughly US$1.27 billion. Trailing net income was US$364 million, so the multiple is about 3.5 times earnings and 0.53 times book. Net cash of about US$861 million covers two-thirds of the market value, which leaves the operating platform priced at roughly US$0.4 billion — near one times its own annual profit. This chapter sizes that discount, checks whether it is FinVolution's alone, and asks how it could pay off.

FinVolution reports in renminbi (¥); the FY2025 Form 20-F translates to US dollars at ¥6.9931 per US$1.00, the December 31, 2025 noon buying rate. Reported financials are shown in ¥, market value and multiples in the currency the ADS trades in — US$. Multiples and percentages are unitless.

The arithmetic of the discount

Trailing P/E (x)

Price / Book (x)

Net cash / market value

Enterprise value / earnings (x)

Source: derived from FY2025 20-F Consolidated Statements of Comprehensive Income [1] and Consolidated Balance Sheets [2], and NYSE market data.

The starting point is what the market pays. FinVolution reported diluted earnings of ¥9.59 (US$1.37) per ADS in 2025 on net income attributable to shareholders of ¥2,542 million (US$364 million) [3]. At US$4.78 that is a trailing multiple of about 3.5 times. Shareholders' equity was ¥16.8 billion (US$2.41 billion) [4], which puts the ADS at 0.53 times book.

The more revealing cut is to strip out the cash. FinVolution held ¥4.29 billion of cash and ¥3.02 billion of short-term investments against about ¥1.28 billion of borrowings — roughly US$861 million of net cash — at the end of 2025 [5]. Subtracting that from the US$1.27 billion market value leaves an enterprise value of about US$409 million for a platform that earned US$364 million last year — an enterprise value near 1.1 times earnings.

Source: derived from FY2025 20-F Consolidated Balance Sheets [6] and NYSE market data; net cash = cash and short-term investments less borrowings.

Read on its own, a business earning US$364 million valued at about US$409 million is the kind of number that either signals mispricing or warns that the earnings are not trusted to last. The rest of the chapter separates those two readings.

A sector discount, not a single-stock one

The first test is whether the market has singled out FinVolution or marked down the whole group. It is the group. The listed Chinese loan-facilitation peers all trade at low-single-digit earnings multiples and well below book, and by mid-2026 several were cheaper than FinVolution on both measures.

Source: market data (Nasdaq/NYSE), approximate, mid-July 2026. Peer multiples are aggregator snapshots and vary by source; X Financial's sub-1x P/E reflects one-off gains, so the price-to-book column is the steadier comparison.

Two things follow. First, the discount is a sector overhang: every one of these China-based, VIE-held consumer lenders is priced at a fraction of book despite reporting profits, which points to shared causes — PRC regulatory and data risk, VIE and delisting fears, and capital-transfer doubts — rather than something specific to FinVolution. Second, FinVolution is not the cheapest name in the group; it sits at the top of the cheap band, at 0.53 times book against roughly 0.16 to 0.44 for the three peers here. That cuts against any claim that the market has uniquely mispriced FinVolution. The more defensible statement is that FinVolution carries a modest premium within a uniformly derated cohort — plausibly for its cleaner balance sheet and its overseas growth (Overseas Engine) — and that a re-rating of the ADS most likely requires the whole sector's discount to lift, not just this one stock's.

The net-cash floor and its asterisk

Two-thirds of the market value in net cash is the bull's anchor, and it deserves a hard look, because cash inside China is not the same as cash a Cayman holding company can hand to ADS holders. FinVolution is explicit that it is "a holding company with no operations of its own," dependent on dividends from its PRC subsidiaries and service fees from the VIEs to fund distributions [7]. The restricted portion is large: paid-in capital, statutory reserves and VIE net assets totaling ¥9.3 billion (US$1.3 billion) were not distributable at the end of 2025, and cash held onshore "may not be available to fund operations or for other use outside of the PRC" [8].

The asterisk is real, but the record argues it is not binding today. FinVolution has in fact moved cash offshore and returned it every year: dividends on the ordinary shares "will be paid in U.S. dollars" [9], the board has declared one every March since 2019, and the US$150 million convertible notes issued in 2025 sit at the holding-company level. So the restriction is a constraint on how fast and how much, not a wall — the discount to net cash is not a claim that the cash is fictional, but a discount for the friction and the tail risk of moving it. A reader who trusts the upstreaming to continue treats the net cash as most of a floor; a reader who prices the SAFE-conversion and policy risk at more than a token haircut does not.

The earnings the multiple sits on

"3.5 times trailing earnings" flatters the entry point, because the trailing year is close to a peak and the near-term direction is down. In the first quarter of 2026 net profit attributable to shareholders fell to ¥415 million (US$60 million) from ¥746 million a year earlier — a 44% drop — as group operating profit slid to ¥547 million from ¥883 million [10]. Consensus carries that through: analysts model earnings per ADS falling about 18% in 2026, to roughly ¥8.3 from ¥10.2, before recovering to about ¥9.7 in 2027.

Sources: FY2023–FY2025 basic earnings per ADS, FY2025 20-F [11]; FY2026–FY2027, consensus estimates.

On the trough year the ADS trades near 4.0 times forward earnings, not 3.5; on the modelled 2027 recovery, back to about 3.4. Neither is expensive, but the distinction matters: this is not a business the market expects to hold its earnings flat and cheap — it is one the market expects to earn less in the year ahead, which is exactly why a low trailing multiple is not, by itself, a margin of safety. The forward decline traces to the same forces earlier chapters set out — a flat, higher-delinquency China book (Guarantee Economics) offset only partly by overseas growth. Against that, the sell-side is more sanguine than the tape: the mean analyst price target sat near US$7.3, roughly 50% above the quote, with six buy ratings and none to sell.

How the discount can pay without a re-rating

If the multiple never expands — the base case when the discount is a sector-wide overhang and there is no takeover or proxy lever to force it (the control picture is in Ownership and Control) — the return has to come from cash. Here the arithmetic is unusually direct. In 2025 FinVolution paid ¥510 million of dividends and repurchased ¥767 million of stock, about ¥1.28 billion (US$183 million) returned in one year against a US$1.27 billion market value [12].

Source: FY2025 20-F Consolidated Statements of Cash Flows [13].

The two channels behave differently, and both help the ADS holder. The dividend is set at 20% to 30% of prior-year net income; the March 2026 declaration was US$0.306 per ADS, a 6.4% yield at US$4.78 [14]. The buyback does something the dividend cannot: because it retires only Class A shares, a fixed dollar profit is spread over a shrinking count, lifting per-ADS earnings and net cash — and it accelerated as the price fell, from 3.6 million ADS at US$9.51 in June 2025 to 4.3 million at US$5.22 that December and 3.6 million at US$5.20 the next month, 18.8 million ADS in all at an average US$6.22 [15]. Buying back stock below book at a mid-teens earnings yield is accretive by construction; the more the discount persists, the more per-ADS value the repurchase transfers to holders who stay.